Large Money Transfers to India: What NRIs Should Know

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

Reviewed for accuracy against primary IRS, FinCEN, and RBI sources. General information, not personal tax or legal advice — confirm your own situation with a qualified professional.

Sending $500 to your parents is one kind of decision. Sending $80,000 for a flat in Bengaluru, or moving a decade of savings back home, is a different animal entirely. The mechanics that don't matter on a small transfer — exchange rate margins, reporting forms, transfer caps, the risk of the rupee moving overnight — suddenly become the whole game. A 1% rate difference that's trivial on $1,000 is ₹68,000 on $80,000. The forms you can ignore on a gift to your mother can carry real penalties on a six-figure move.

None of it is hard once you know what to watch. But large transfers reward planning in a way small ones don't, and the people who wing it tend to leave money on the table or stumble into a compliance question they didn't expect. Here's how to do it cleanly.

First, the limits question

The most common worry: "Is there a cap on how much I can send to India?" For sending money from the US to India, there's no single legal ceiling on personal remittances. You're not breaking a rule by sending a large amount. What you'll actually run into are two practical limits.

The first is your transfer service's own caps. Every app and bank sets per-transfer, daily, and annual limits, and they rise as you complete more identity verification. A new, lightly verified account might cap you at a few thousand dollars; a fully verified one can go far higher. If you're planning a large send, complete full verification before you start, so you don't hit a wall halfway through.

The second is the money coming back the other way. If you're an NRI moving money out of India — repatriating — that's where the real cap lives: up to USD 1 million per financial year from an NRO account, with specific forms required. That's covered separately in how to repatriate money from India to the USA. For sending into India, the limits are practical, not legal.

The reporting forms that can apply

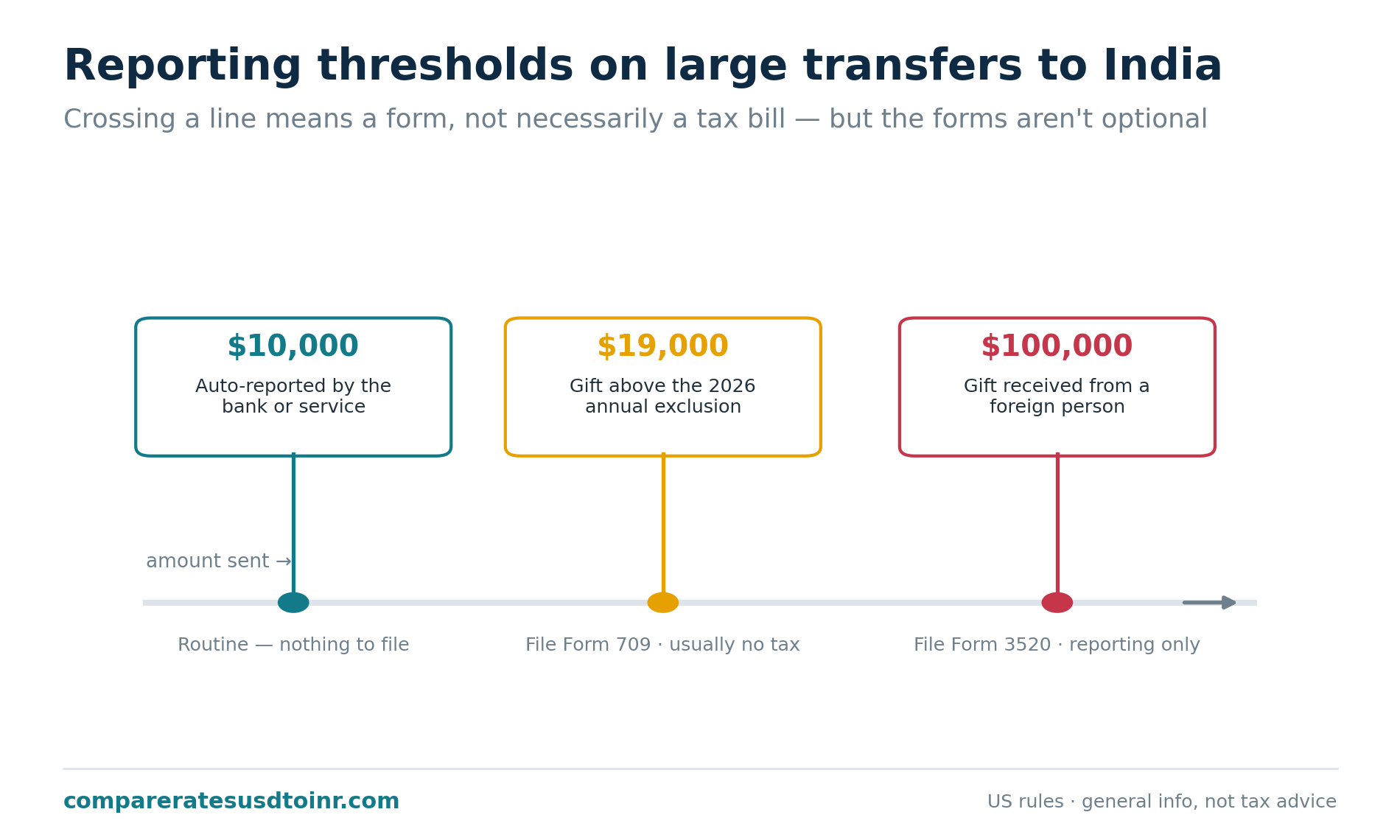

This is where large transfers differ most from small ones, and where a little knowledge prevents a lot of stress. Nothing here usually means you owe tax — it's mostly about reporting. But the forms are not optional when their thresholds are crossed.

On the US side, if you're gifting: US citizens and residents can give up to the annual gift tax exclusion per recipient per year without any filing — that figure is $19,000 for 2026. Give more than that to one person in a year and you're expected to file IRS Form 709. Here's the relief: filing Form 709 almost never means paying tax. It just uses up a sliver of your very large lifetime gift/estate exemption (in the millions). So a parent gifting $50,000 to a child files the form but typically owes nothing. It's paperwork, not a tax bill. Splitting a gift between two spouses as givers, or across two recipients, can also keep you under thresholds — more in NRI tax rules on money sent to India.

On the US side, if you're receiving from India: if you receive gifts totaling more than $100,000 from a foreign person (like a parent in India) in a year, you must file IRS Form 3520. Again, it's a reporting form, not a tax — but the penalties for not filing are steep, so it matters. This comes up for NRIs receiving an inheritance or a large family gift from India. See FBAR and Form 3520.

Automatic bank reporting: any international transfer over $10,000 is reported by the financial institution to the authorities automatically. You don't file anything for this — it happens in the background — and it's completely routine. It's not a red flag; it's just standard anti-money-laundering record-keeping. Don't try to dodge it by splitting transfers into sub-$10,000 chunks; deliberately structuring transfers to avoid reporting is itself a violation, and it's pointless since legitimate transfers have nothing to hide.

On the India side: money received as a gift from a close relative is generally not taxable in India, regardless of size. So your parents receiving a large gift from you typically owe no Indian tax on it. Gifts from non-relatives above ₹50,000 in a year can be taxable to the recipient, but family support usually falls in the exempt category.

| Situation | Form / rule | Usually owe tax? |

|---|---|---|

| You gift over $19,000 (2026) to one person | IRS Form 709 | No — uses lifetime exemption |

| You receive over $100,000 from a foreign person | IRS Form 3520 | No — reporting only |

| Any transfer over $10,000 | Auto-reported by the bank | No — routine |

| Indian relative receives your gift | India: exempt for close relatives | No (close relatives) |

The cost that dwarfs everything: the exchange rate

On a large transfer, the exchange rate margin is the single biggest cost, and it's the one most people underestimate because it's invisible. A bank quietly taking a 2% markup on $80,000 keeps roughly ₹1,36,000 — far more than any visible fee. Shopping the rate carefully, which barely matters on $500, is worth serious effort on a large sum.

For big amounts, you have leverage you don't have on small ones. Some banks and specialist services will negotiate a tighter rate for large transfers, especially if you ask or if you're a priority customer. Specialist foreign-exchange brokers, built for larger sums, often beat both banks and consumer apps once you're into the tens of thousands. And the delivered-rupees comparison from how much INR you'll receive after fees becomes essential — at this scale, a careful comparison can be worth lakhs.

Protecting against the rupee moving

There's a risk on large transfers that doesn't exist on small ones: timing exposure. If you're buying property and the deal closes in two months, the rupee could move 2–3% against you before you transfer, swinging the cost by ₹1,50,000+ on a large purchase. You're carrying currency risk whether you think about it or not.

Two tools help. A forward contract lets you lock today's rate for a transfer you'll make later, removing the uncertainty entirely — you know exactly what it'll cost regardless of where the rupee goes. A rate lock feature in some apps does a lighter version of the same thing for a short window. You give up the chance of a better rate in exchange for certainty, which is usually the right trade when a large, time-sensitive sum is at stake. We cover both in forward contracts and rate locks for NRIs.

If you'd rather not lock, splitting a large transfer into a few tranches over several weeks at least protects you from converting the entire amount on the single worst day. It doesn't improve your average rate, but it caps your regret.

A property-closing scenario, start to finish

Walk through a realistic case, because it ties the pieces together. Arjun, an NRI in Chicago, is buying a flat in Pune for the rupee equivalent of about $90,000, with the deal closing in roughly eight weeks. Here's how a careful version of this plays out.

He starts by getting his accounts in order. The money will flow through his NRE account, since it's foreign earnings going into India, which keeps it cleanly repatriable if he ever sells — important, because property bought with NRE funds has friendlier resale-repatriation treatment. He fully verifies his transfer accounts now, weeks ahead, so he won't hit a limit when the clock is ticking.

Next he confronts the timing risk. Over eight weeks, the rupee could easily move 2–3% — on $90,000, that's a swing of well over ₹1,50,000 either direction. Rather than gamble on it, he locks a rate through a forward contract for the bulk of the amount, so the cost is fixed regardless of where the rupee goes by closing day. He sleeps better, and the budget stops being a moving target.

He shops the rate hard, because at this size the margin is the whole game. He gets quotes from his bank, a consumer app, and a specialist FX broker, and compares delivered rupees — the broker, built for large sums, comes out ahead by enough to matter. On the reporting side, since he's sending his own money to his own account rather than gifting, the US gift forms don't apply, but the transfer is auto-reported over $10,000 as routine, and he keeps every confirmation for his records. When closing day arrives, the rate is already locked, the account is ready, and the transfer goes through without drama. That's what planning buys you on a large transfer: no surprises.

Record-keeping that saves you later

Large transfers are exactly the ones a tax authority or bank might ask about years later, so keep a clean paper trail. Save the transfer confirmation, the rate you received, the purpose of the transfer, and — for gifts — a simple note of who gave what to whom. If you filed Form 709 or Form 3520, keep copies with your tax records. For property, hold onto the source-of-funds documentation, because it matters when you eventually sell and want to repatriate the proceeds. None of this is onerous, and it turns a potentially stressful future question into a two-minute lookup.

Practical steps for a clean large transfer

A sensible sequence for, say, a $50,000+ move: verify your transfer account fully in advance so limits aren't a surprise. Decide whether the timing risk justifies locking a rate, especially if the transfer is tied to a deadline like a property closing. Get rate quotes from at least two or three sources — your bank, a consumer app, and a specialist FX broker — and compare delivered rupees, not fees. Confirm whether any reporting form applies on your side (Form 709 if you're gifting above the exclusion, Form 3520 if you're receiving a large foreign gift), and keep records. Then execute, and hold onto the confirmation and rate details for your tax file.

For property specifically, there are extra account and repatriation considerations worth reading first — see sending money to India for property purchase. And if the destination is your own account in India, get the NRE/NRO choice right per NRE vs NRO accounts explained, since it affects how easily you can move the money back later.

If you're new to sending money to India at all, the complete guide to sending money from the USA to India and best ways to send money from USA to India cover the fundamentals this article builds on. To compare providers on the one number that matters, use how much INR you'll receive after fees. And because a large transfer's timing risk can swing the cost by lakhs, it helps to understand what actually moves the rupee, laid out in USD to INR forecast and key drivers, before deciding whether to lock a rate.

Sources & further reading

- IRS — Frequently Asked Questions on Gift Taxes (annual exclusion)

- IRS — About Form 709, U.S. Gift (and GST) Tax Return

- IRS — Gifts from Foreign Person (Form 3520 reporting)

- FinCEN — Bank Secrecy Act (currency transaction reporting & anti-structuring)

- Reserve Bank of India — FAQs on Remittance Facilities / NRI repatriation

Frequently asked questions

Is there a limit on sending money to India? There's no single legal cap on sending personal money from the US to India. The practical limits are your transfer service's own per-transfer and annual caps (which rise with identity verification) and any US gift-reporting thresholds. Moving money out of India is where the firm USD 1 million-per-year repatriation cap applies.

Do I report a large transfer to the IRS? Transfers over $10,000 are automatically reported by the bank or service — you don't file anything. If you gift more than the annual exclusion ($19,000 in 2026) to one person, you file Form 709 (usually no tax owed). If you receive over $100,000 from a foreign person, you file Form 3520 (reporting only).

How much money can I send to parents in India tax-free? Gifts to close relatives are generally exempt from tax in India for the recipient, regardless of amount. On the US side, you can gift up to the annual exclusion ($19,000 in 2026) per recipient without filing; above that you file Form 709 but typically owe no tax, as it draws on your large lifetime exemption.

Should I split a large transfer? Splitting to manage rate risk across dates is fine. But never split transfers specifically to stay under the $10,000 reporting threshold — deliberately structuring transfers to avoid reporting is illegal and pointless, since legitimate transfers are reported routinely with no consequence.

General information, not tax, legal, or financial advice. Thresholds and rules change and depend on your circumstances — consult a qualified tax professional for large transfers.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.