How Much INR Will You Receive After Fees in 2026?

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

Quick puzzle. You send $1,000. Google says the rate is ₹86, so you tell your brother to expect ₹86,000. He texts back: "Got ₹84,200." Did someone cheat you?

No. You just did the math the way the marketing wants you to — using the headline rate and ignoring everything between the dollar leaving your account and the rupee landing in his. The gap, ₹1,800 in this case, is the total cost of the transfer, and it's made of two parts that hide in different places. Once you can break that ₹1,800 into its pieces, you can predict the delivered amount for any service, and pick the one that actually gives your family the most.

The two numbers that decide everything

Every USD→INR transfer comes down to two figures: the rate you're given and the fee you're charged. That's it. Master those two and you can compute the landed rupees yourself, every time.

The rate is the bigger lever. The "real" rate — the mid-market rate, the one on Google — is almost never the rate you get. Services shave a margin off it. So the rate you're given is the mid-market rate minus their markup. If mid-market is ₹86.00 and a service marks it down by 1%, your rate is ₹85.14.

The fee is the smaller, more visible lever — the explicit charge, often $0 to $8 for apps, $25 to $45 for bank wires.

The delivered rupees come from applying both:

INR received = (USD sent − fee in USD) × rate given

Let's run our example. $1,000 sent, $5 fee, and a rate of ₹85.14 (mid-market ₹86 minus a 1% markup):

(1000 − 5) × 85.14 = 995 × 85.14 = ₹84,714

Compared against the ₹86,000 you'd get at a perfect rate with no fee, the transfer cost ₹1,286. Of that, only ₹5 worth (about ₹425) was the visible fee. The other ₹860 was the markup you never saw. That ratio — most of the cost hiding in the rate — is typical.

Why "same rate, different rupees" happens

This is the puzzle that makes people suspicious. Two apps both say "₹85.50" and yet deliver different amounts. Usually one of three things is going on.

First, the fee differs. Same rate, but one charges $3 and the other $8 — that's $5, around ₹425, gone on a $1,000 send.

Second, one quote includes the fee in the displayed rate and the other doesn't, so you're not comparing like with like. Always check whether the rate shown is before or after fees.

Third — and this is the sneaky one — the funding method differs. The "₹85.50" you saw might be the bank-funded rate, but you're paying by card, which carries a worse rate or an extra charge. Same app, same screen, different real cost depending on how you pay. We get into that in hidden fees in USD to INR transfers.

The fix for all three: stop comparing rates and fees separately. Compare the one number that already combines them — the delivered rupees.

Worked comparison: three services, one $1,000 transfer

Assume mid-market is ₹86.00 and you're funding from your bank account. Watch how the delivered figure, not the headline, sorts them out.

| Service | Markup | Rate given | Fee | Delivered INR | Total cost vs perfect |

|---|---|---|---|---|---|

| Service A ("no fee") | 2.0% | ₹84.28 | $0 | ₹84,280 | ₹1,720 |

| Service B (transparent) | 0.4% | ₹85.66 | $6 | ₹85,148 | ₹852 |

| Service C (bank wire) | 1.8% | ₹84.45 | $30 | (1000−30)×84.45 = ₹81,917 | ₹4,083 |

Service A shouts "no fee" and still costs more than twice what Service B costs, because its markup is large. Service B charges a visible $6 and wins comfortably. The bank wire, with both a big fee and a markup, is the worst by a wide margin — and that's before any correspondent-bank or receiving-side charges, which would make it worse still. The delivered column tells the whole truth; the "no fee" badge tells you almost nothing.

A pocket method you can do in your head

You don't need a spreadsheet at the counter. Here's a fast mental version.

Take the mid-market rate from Google. Knock off roughly the markup percentage you suspect, then subtract the fee. For a quick gut check, remember that every 1% of markup on a $1,000 transfer is about ₹860, and a $5 fee is about ₹425. So a "no fee, 2% markup" offer costs you around ₹1,720, while a "$6 fee, 0.4% markup" offer costs around ₹850. The second is cheaper despite charging a visible fee. Do this rough sum and the marketing loses its power over you.

For larger amounts, scale it linearly: 1% markup on $10,000 is about ₹8,600, which is why on big transfers the markup matters enormously and a small fee becomes a rounding error. That's the core insight behind markup vs transfer fee.

Keep two reference numbers in your head and you can sanity-check almost any offer on the spot: roughly ₹860 per 1% of markup on $1,000, and about ₹85–86 per dollar of fee at typical rates. With just those two, you can take any "$X fee, Y% markup" pitch and turn it into a rupee cost in seconds, no app required. A service quoting a $0 fee but a 1.5% markup on a $1,000 send is costing you about ₹1,290; a rival at a $7 fee and 0.3% markup costs about ₹600 plus ₹260, roughly ₹860 — cheaper, despite the visible fee. The mental shortcut does the same work the formula does, just faster, and it's enough to keep you from being talked into a worse deal at the counter.

The same math at two different sizes

The reason this formula is worth internalizing is that the winner changes with the amount, and only the delivered-rupees math reveals it.

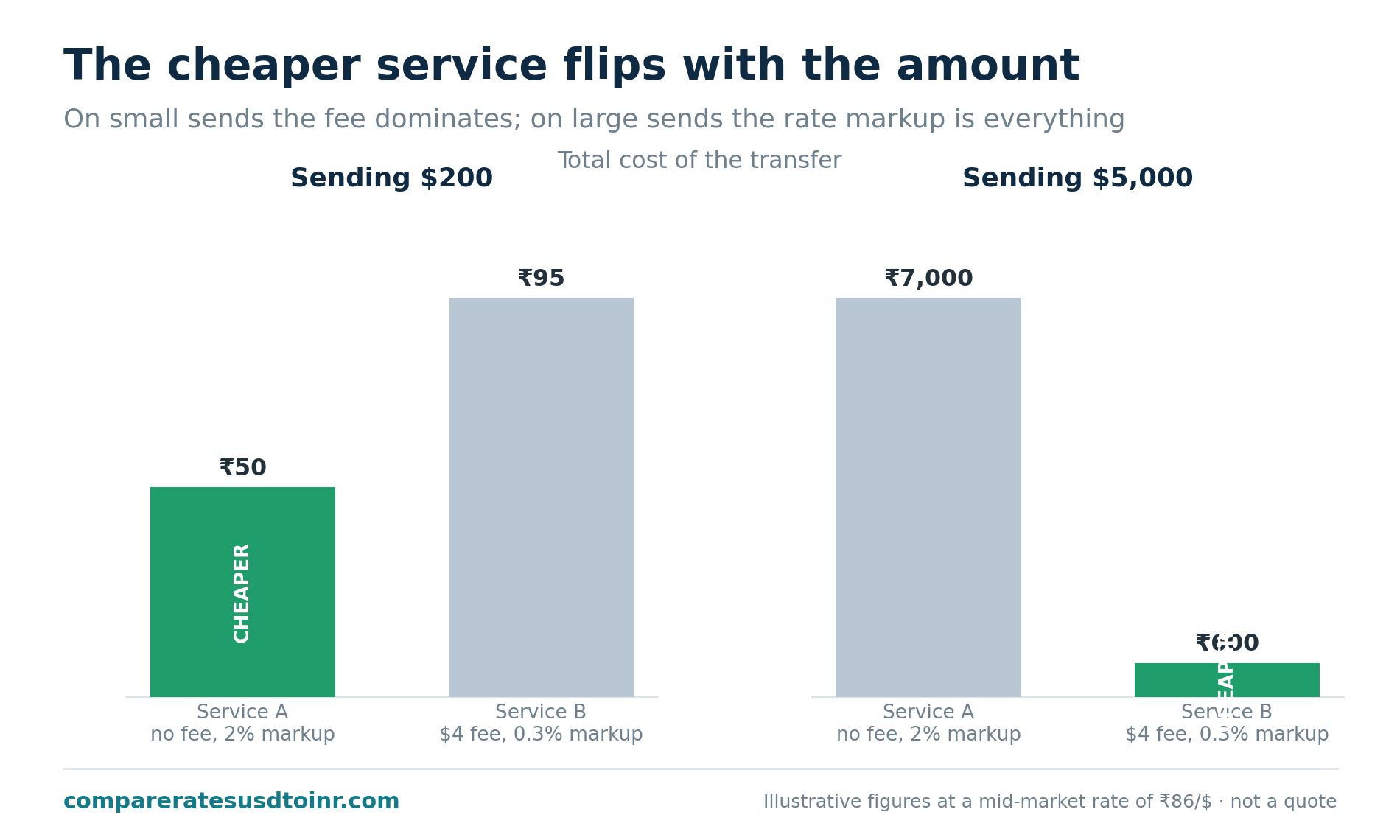

Take a small transfer, $200, with mid-market at ₹86. Service A charges no fee but a 2% markup; Service B charges a $4 fee with a 0.3% markup. Service A delivers 200 × 84.28 = ₹16,856. Service B delivers (200 − 4) × 85.74 = ₹16,805. On $200, Service A — the "no fee" one — actually wins by about ₹50, because the markup on such a small amount is tiny in rupees while the $4 fee bites proportionally harder.

Now scale up to $5,000, same two services. Service A delivers 5000 × 84.28 = ₹4,21,400. Service B delivers (5000 − 4) × 85.74 = ₹4,28,357. Service B wins by nearly ₹7,000, because at this size the 2% markup is enormous and the $4 fee is trivial. Same two services, opposite winners, decided entirely by amount. If you'd picked a provider based on your last $200 transfer and stuck with it for a $5,000 one, you'd have left ₹7,000 on the table. The formula is what protects you from that — run it at the amount you're actually sending, every time.

A faster way: reverse-engineer the markup

Here's a shortcut for sizing up any service. Take the rupees it promises to deliver, add back the fee in rupees, and divide by your dollars — that gives you the effective rate you're actually getting. Compare that against the mid-market rate, and the gap is the markup percentage.

For example, a service promises ₹84,714 on $1,000 with a $5 fee. Add the fee back: ₹84,714 + (5 × 86) ≈ ₹85,144. Divide by $1,000 = ₹85.14 effective rate. Against a mid-market of ₹86.00, that's a markup of about 1%. Now you can compare that 1% against a rival's markup directly, apples to apples, no matter how each dresses up its pricing. This is the single most useful trick for cutting through "no fee" marketing — it converts every offer into one comparable number.

Don't forget the receiving end

The formula above assumes nothing is deducted in India. For app transfers that guarantee a delivered amount, that's usually safe — the figure they quote is what lands. For bank wires, it isn't. A correspondent bank in the middle can take a lifting fee, and the recipient's bank may charge for processing an inbound foreign remittance. Those come out after your math, so the real landed figure can be lower than your calculation suggests.

This is a strong argument for using services that promise an exact delivered amount: the number they show is the number your family gets, with no surprises on their end. With a raw wire, build in a buffer for charges you can't see, which is one more reason apps tend to win for ordinary transfers — see why banks give worse exchange rates.

Putting it to work

Next time you're about to send, do this. Note the mid-market rate. Open the two services you're choosing between, enter your exact amount and the funding method you'll actually use, and read the delivered-INR figure each promises. Pick the larger. If you want to verify a service isn't quietly inflating its markup, plug its numbers into the formula — (USD − fee) × rate given — and compare the result against what it claims to deliver. They should match. If a wire is involved, shade your estimate down for unseen charges.

That's the entire skill. Not predicting rates, not decoding marketing — just computing the one honest number and choosing the bigger one. For the broader strategy on picking a provider, see best ways to send money from USA to India, the full complete guide to sending money from the USA to India, and for the apps head-to-head, Wise vs Remitly vs Xoom.

Where the math matters most

This calculation earns its keep on bigger transfers. On $200, the difference between a good and bad provider might be ₹100 — worth a glance, not an investigation. On $20,000, the same percentage gap is ₹17,000, which is worth ten minutes of careful comparison. So scale your effort to the stakes: a quick check for small sends, a thorough delivered-rupees comparison across two or three services for anything large. The framework in large money transfers to India builds on exactly this math for high-value transfers, where the rate margin becomes the dominant cost.

The same arithmetic also explains why banks tend to lose — they stack a fee and a markup, and often a correspondent charge on top, as broken down in why banks give worse exchange rates than remittance apps. And if you want to see every place a cost can hide before it reaches your formula, hidden fees in USD to INR transfers is the companion piece. Run the numbers, trust the delivered figure, and no marketing claim can mislead you.

Sources & further reading

- Wise: How we make money (and our pricing)

- Remitly Fees and Pricing (Help Center)

- Reserve Bank of India: Liberalised Remittance Scheme (FAQs)

- Consumer Financial Protection Bureau: What is a remittance transfer?

- Investopedia: Mid-Market Rate

Frequently asked questions

How do I calculate INR received after fees? Use: INR received = (USD sent − fee in USD) × rate given. The "rate given" is the mid-market rate minus the service's markup, which is usually a bit worse than the rate on Google. The delivered figure, not the headline rate, is what matters.

Why did I receive less INR than quoted? Most likely because the quote used the mid-market rate while the service applied a markup, charged a fee, or both. For bank wires, correspondent and receiving-bank charges can also reduce the landed amount after the conversion. Compare the delivered-INR figure, and prefer services that guarantee it.

What is the mid-market rate? The mid-market rate is the midpoint between the buy and sell prices in the currency market — the "real" rate you see on Google. It's the benchmark, but almost no consumer service gives you exactly that rate; they add a markup. See our explainer on the mid-market rate.

Does the recipient pay any fees in India? With app transfers that guarantee a delivered amount, usually no — the quoted figure is what lands. With bank wires, the recipient's bank may charge a fee for an inbound foreign remittance, and a correspondent bank may have already taken a cut in transit.

General information, not financial advice. Example rates are illustrative and change daily. Confirm live figures with your provider before sending.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.