Best Ways to Send Money from USA to India in 2026

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

My uncle still walks into his bank branch in New Jersey, fills out a wire form by hand, and pays $45 to send money to his daughter in Pune. He's convinced it's the "safe" way. Last time I checked his transfer against an app on my phone, the bank had quietly handed him about ₹2,800 less on a $1,000 transfer than the app would have. The wire fee was the part he could see. The exchange rate was where the real money leaked out.

That gap — between what feels safe and what actually costs the least — is the whole story of sending money home. The good news is that the cost of a transfer from the USA to India has dropped a lot over the past decade, and the tools have gotten genuinely good. The trick is knowing which tool fits which situation, because the "best" way changes depending on how much you're sending, how fast it needs to land, and how the recipient wants to receive it.

The four routes your dollars can take

Strip away the branding and almost every option falls into one of four buckets.

The first is your bank's wire transfer. It works, it's secure, and it's almost always the most expensive route for amounts under a few lakh rupees. You pay an upfront wire fee, the recipient's bank often skims a charge of its own, and the exchange rate the bank uses tends to sit well below the real market rate. For most people sending money to family, this is the option to avoid unless you have a specific reason to use it.

The second is a specialist money transfer app — Wise, Remitly, Xoom, Instarem, and a handful of others. These were built for exactly this job. They tend to give rates close to the real market rate, charge transparent fees, and deliver to an Indian bank account in anywhere from a few minutes to a couple of days. For the vast majority of personal transfers, one of these will be your answer.

The third is a money transfer operator with a retail network, like Western Union or Ria. Their edge is reach: cash pickup at thousands of locations across India, which matters if your recipient doesn't have a bank account or needs physical cash in a small town. You usually pay for that convenience through a wider rate margin.

The fourth, often overlooked, is the NRE/NRO account route — moving money into your own Non-Resident account in India, sometimes via the same apps, sometimes via specialist remittance arms of Indian banks like ICICI Money2India or SBI's remittance service. If you're sending money to yourself rather than to family, this changes the math, because tax treatment and repatriation rights come into play. Our guide to NRE vs NRO accounts digs into that side.

What "cheapest" actually means

Here's the part that trips up almost everyone. When you compare two services, the advertised fee is the smallest piece of the puzzle. The bigger lever is the exchange rate.

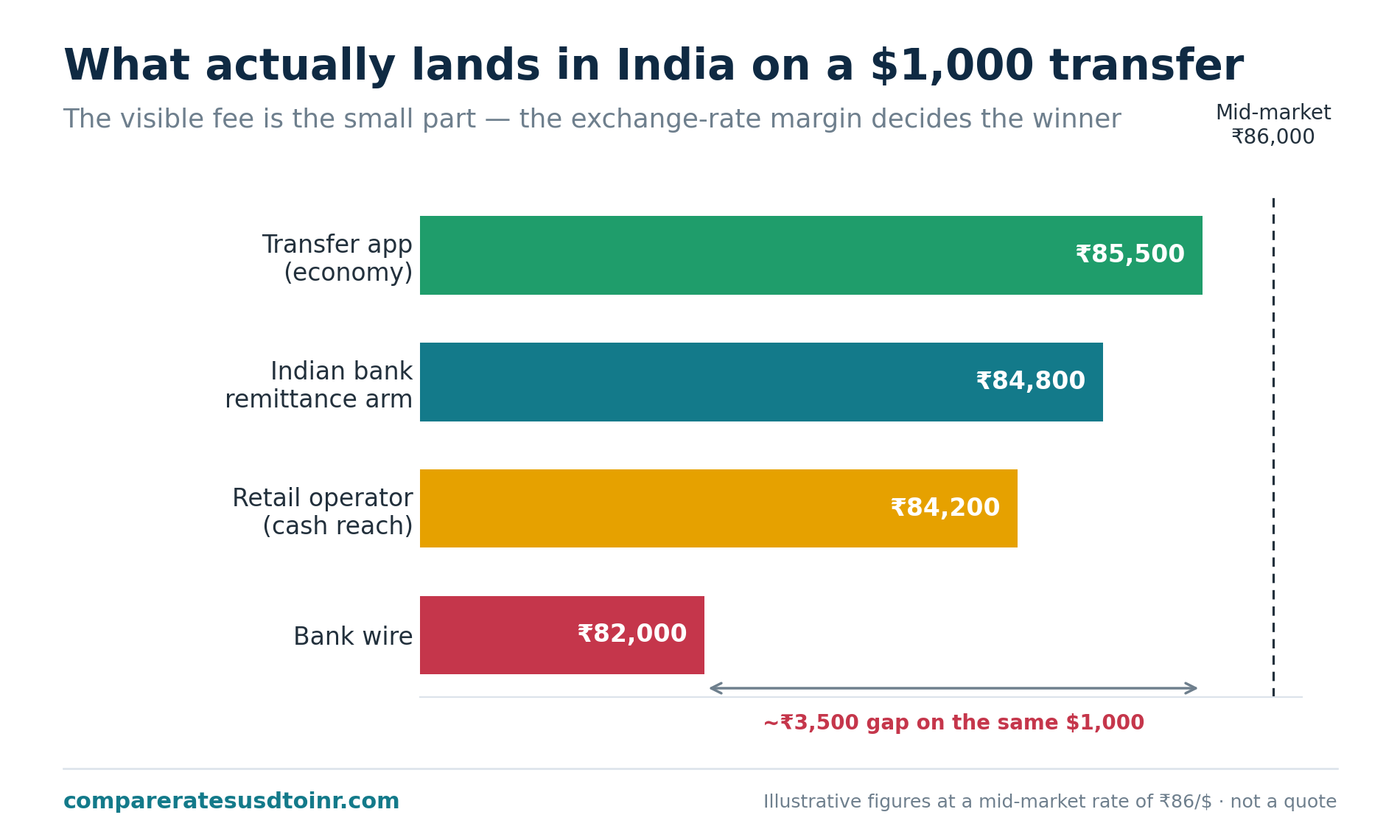

Picture the real market rate — the one you'd see if you searched "USD to INR" on Google — sitting at ₹86 to the dollar. That's called the mid-market rate, and it's the midpoint between what buyers and sellers are trading at. Almost no consumer service gives you that exact number. Instead, they shave a margin off it. One app might give you ₹85.70. Your bank might give you ₹84.20. On a $1,000 transfer, that difference alone is ₹1,500 — and you'd never see it as a line item.

So the real cost of any transfer is two things added together: the fee you pay, plus the gap between the market rate and the rate they actually give you. A service charging a $3 fee with a near-perfect rate will usually beat a "zero fee" service that buries a 2% margin in the exchange rate. We walk through that comparison properly in markup vs transfer fee, but the one-line version is: always compare the final rupees that land in India, not the fee.

To make this concrete, here's roughly how a $1,000 transfer shakes out across the four routes. Treat these as illustrations — actual numbers shift daily.

| Route | Typical upfront fee | Rate vs market | Rough INR delivered on $1,000 | Speed |

|---|---|---|---|---|

| Bank wire | $25–$45 | 1.5%–3% below | Lowest of the four | 1–3 business days |

| Transfer app (Wise/Remitly economy) | $0–$8 | 0.4%–0.9% below | Highest of the four | Minutes to 2 days |

| Retail operator (Western Union/Ria) | $0–$5 | 1%–2.5% below | Middle | Minutes (cash) to 1 day |

| Indian bank remittance arm | $0–$10 | varies, often 0.5%–1.5% | Middle to high | 1–4 days |

The pattern holds across amounts: apps win on cost for ordinary transfers, banks lose, and retail operators earn their keep only when you need cash pickup or reach into places apps don't serve.

Matching the method to the situation

Cost isn't the only thing that matters, which is why there's no single winner. A few common situations, and what I'd actually reach for:

Monthly support to parents, going into their bank account. This is the bread-and-butter case. A transfer app with an economy/bank-funded option is almost always best. ACH funding (pulling from your US checking account) is cheaper than card funding, even though it's a day or two slower. Set it and forget it. If you're doing this every month, see recurring transfers to India for a way to automate without overpaying.

You need it there today, and it's urgent. Remitly's "Express" tier, Xoom, and a few others can deliver to a bank account in minutes. You pay slightly more for the speed — a wider margin or a small fee — but when a hospital bill is due, that's a fair trade.

The recipient wants cash, or lives somewhere rural. Cash pickup through Western Union or Ria is the practical choice. UPI-linked transfers are also worth checking now, since several apps deposit directly to a UPI ID. We compare these in cash pickup vs bank deposit.

A large, one-time sum — say, helping with a property down payment or moving savings home. Here the exchange rate margin dwarfs everything else, because a 1% difference on $50,000 is ₹40,000+. This is where it pays to shop the rate carefully, consider a rate lock, and understand the reporting side. Large money transfers to India covers the limits and paperwork.

The traps that quietly cost you

A few things consistently catch people out.

Funding with a credit card. Most apps charge noticeably more for card payments, and your card issuer may treat it as a cash advance with its own fee and interest. Bank/ACH funding is almost always the cheaper path if you can wait the extra day.

Trusting the "you save $X" banner. Comparison banners inside an app are marketing. The only honest comparison is the final INR figure across two or three services at the same moment, for the same amount and funding method.

Forgetting the receiving side. Some routes deduct a charge on the India end, or the recipient's bank applies one. Apps that promise the recipient gets the full amount are clearer here, but it's worth confirming once.

First-transfer rates. New customers often get a sweetheart rate or a waived fee on the first send. It's real, but it expires. Don't pick a long-term provider based on a one-time promo — judge it on the ongoing rate.

Limits you didn't know about. Each service caps how much you can send per transfer, per day, and per year, and those caps depend on how much identity verification you've completed. If you're sending a big sum, check the ceiling before you start, or you'll hit a wall mid-transfer.

A simple routine that beats most people

You don't need to become a currency trader. A light routine handles 95% of cases well.

Keep two transfer apps installed, not one. Before any meaningful transfer, open both and check the actual rupees delivered for your exact amount and funding method. It takes ninety seconds and the winner flips more often than you'd expect, especially around promotions and weekends. Fund from your bank account rather than a card whenever time allows. And for anything large or time-sensitive, slow down for a moment and read the section above that matches your situation, because the default "cheapest app" answer doesn't always apply.

If you want the deeper version of any piece of this, a few articles go further: Wise vs Remitly vs Xoom for a head-to-head on the three biggest apps, how to compare money transfer rates to India for the method, hidden fees in USD to INR transfers for everything that hides in the rate, and how much INR you'll receive after fees for the actual arithmetic.

Is it safe to send money online?

Worth addressing directly, because it's the reason my uncle clings to his branch. The major apps are licensed money transmitters, regulated state by state in the US and registered with FinCEN, and they move enormous volumes daily. Your money is no less safe with a reputable app than with a bank wire — arguably safer, since you get live tracking and a clear record. The real risks are the ordinary ones: sending to the wrong account number, or falling for a scam where someone pressures you to send money to a stranger. Double-check the recipient details, and never send money to someone you haven't verified, no matter how urgent they make it sound.

What to expect after you hit send

The first transfer through any new service is almost always the slowest and most nerve-wracking, and it's worth knowing why so you don't panic. New accounts go through identity verification, and a first send — especially a larger one — can get held for review for a few hours or even a day while the service confirms you are who you say you are. This is normal, it's a sign the service takes fraud seriously, and it usually never happens again. If you're sending something time-sensitive, do a small test transfer first to clear verification, then send the real amount.

Once you're an established customer, transfers settle into a rhythm. Bank-funded sends take a day or two because the ACH pull from your US account is the slow link, not the payout in India. The money leaving your account and the money arriving in India are two separate legs, and the app will show you both. Good apps give you live tracking and a notification when the funds land — keep an eye on it for the first few transfers until you trust the timing.

One habit that saves grief: confirm the very first transfer to a new recipient with a tiny amount, say $20, and have them check it actually arrived in the right account before you send the full sum. Account numbers and IFSC codes are easy to mistype, and a small test catches an error while it's still cheap to fix. After that first confirmation, you can save the recipient and send larger amounts with confidence.

Sources & further reading

- FinCEN — Money Services Business (MSB) Registration

- IRS — Gift Tax and Form 709 Instructions

- Reserve Bank of India — Liberalised Remittance Scheme (FAQs)

- Wise — How fees and the mid-market exchange rate work

- Consumer Financial Protection Bureau — Sending money internationally

Frequently asked questions

What is the cheapest way to send money to India? For most personal transfers into an Indian bank account, a transfer app's economy/bank-funded option (Wise, Remitly economy, Instarem) is cheapest, because it pairs a small transparent fee with a rate close to the real market rate. Bank wires are usually the most expensive once you account for the rate margin.

How long does a transfer from the USA to India take? Anywhere from a few minutes to three business days. Express tiers and cash pickup can be near-instant; economy bank-funded transfers typically take one to two days because the ACH pull from your US account is slower.

Is it safe to send money to India online? Yes, when using a licensed, established provider. The main risks are user errors — wrong account details — and scams, not the technology. Verify the recipient and avoid anyone pressuring you to send money urgently.

How much money can I send to India in a year? There's no single legal cap on personal remittances, but each service sets its own limits, and large gifts can trigger US reporting (Form 709 above the annual gift exclusion, and the recipient side rarely owes Indian tax on gifts from close relatives). See large money transfers to India and NRI tax rules.

This article is general information, not financial or tax advice. Exchange rates, fees, and service features change frequently — confirm current figures with the provider before you transfer.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.