USD to INR Forecast 2026: What Actually Moves the Rupee

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

There's a graveyard of confident rupee forecasts. Every January, analysts publish targets for where USD/INR will sit by December, and most years reality wanders somewhere they didn't predict, for reasons that seemed obvious only in hindsight. So if you came here for a number — "the rupee will be at X by next quarter" — I'd gently steer you away from anyone who offers one with certainty, including me.

What's far more useful, and actually knowable, is why the rupee moves. The forces are a short, understandable list. Once you can read them, you'll understand the headlines, you'll stop being surprised by big moves, and you'll make better decisions about your own transfers than someone clinging to a forecast. So let's skip the crystal ball and look at the machinery.

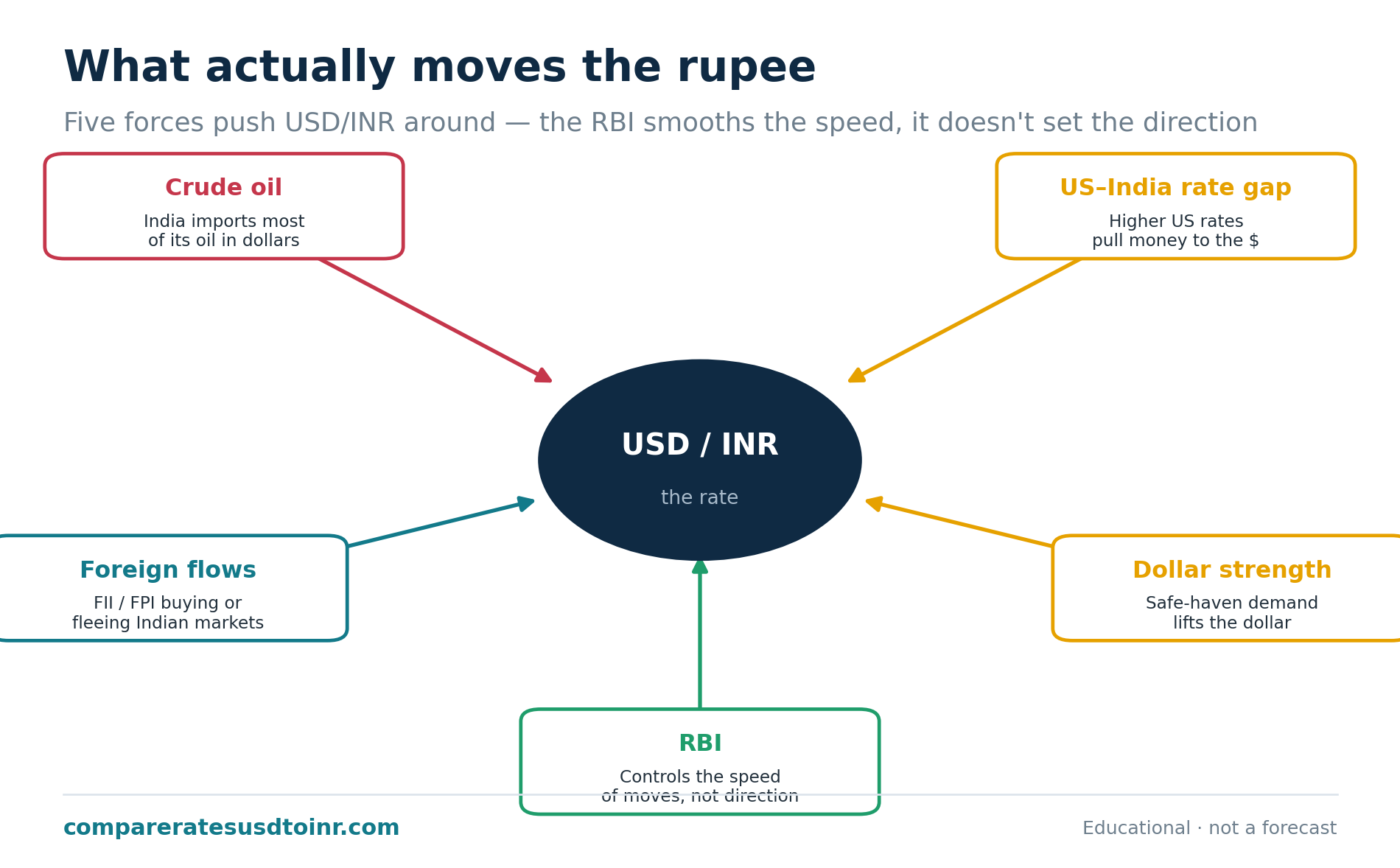

The five forces that move the rupee

1. Crude oil. This is the big one for India, and it's worth understanding deeply. India imports the large majority of the oil it burns, and it pays for that oil in dollars. When crude prices rise, India needs more dollars to buy the same amount of oil, which means selling more rupees to get those dollars — and that pushes the rupee down. The relationship is almost mechanical: a sustained spike in Brent crude tends to feed quickly into a weaker rupee. If you want one indicator to watch as an NRI, oil is it. A geopolitical shock that sends crude soaring is bad news for the rupee; a calm, cheap-oil environment supports it.

2. The interest rate gap. Money flows toward higher returns. When US interest rates are high relative to India's, holding dollars becomes more attractive, capital flows toward the US, and the rupee tends to soften. When that gap narrows — US rates falling, or India's holding firm — some of that pressure eases. This is why everyone watches the US Federal Reserve so closely: its rate decisions ripple straight into emerging-market currencies like the rupee.

3. Foreign investment flows. Global investors pour money into Indian stocks and bonds when they're optimistic, and yank it out when they're nervous. Those flows are huge and fast. When foreign investors are buying Indian assets, they're buying rupees to do it, which supports the currency. When they flee to safety during global stress, they sell rupees, and the currency drops. India's inclusion in global bond indices has added a new, more stable source of inflows, but sentiment-driven money can still swing the rupee sharply in either direction over short periods.

4. The dollar itself. Sometimes the rupee falls not because anything changed in India, but because the dollar is strong against everything. When global investors get fearful, they rush into the US dollar as a safe haven, and that broad dollar strength drags the rupee down along with most other currencies. It's worth separating "the rupee is weak" from "the dollar is strong" — they look identical on a USD/INR chart but have different causes and different likely durations.

5. The Reserve Bank of India. The RBI doesn't set the exchange rate, but it manages how fast it moves. It holds a large pile of foreign-exchange reserves and uses them to smooth out sharp swings — selling dollars to support the rupee when it's falling too quickly, buying them when it's rising. The key mental model: the RBI controls the speed of the move, not its direction. If the underlying forces are pushing the rupee down, the RBI can slow the slide and prevent panic, but it generally won't reverse a fundamental trend, because fighting the fundamentals burns reserves fast.

How these forces combine in practice

Rarely does just one force act at a time, which is why forecasting is so hard. A realistic scenario: oil spikes (rupee pressure down) at the same time US rates stay high (more pressure down) while foreign investors get nervous and pull money out (still more pressure down). All three lean the same way, the rupee weakens sharply, and the RBI steps in to slow it rather than stop it. That's roughly the recipe behind most of the rupee's big down-moves.

The reverse can happen too: oil falls, the US starts cutting rates, foreign money flows into Indian bonds, and the dollar softens globally. Stack those up and the rupee firms. The trouble is that these forces don't move in unison or on schedule, and a single surprise — a conflict, an oil shock, a sudden shift in Fed expectations — can flip the balance in a week. That's the honest reason precise forecasts keep failing.

The long-run picture vs the short-run noise

Step back far enough and there's a gentle, persistent trend: the rupee has weakened against the dollar over the long run, gradually, with plenty of bumps. This isn't a crisis; it reflects structural factors like India's higher inflation relative to the US and its standing as a net oil importer. For an NRI, the practical takeaway is that holding rupees over many years has tended to lose a little against the dollar on average — which matters for decisions like parking savings in Indian deposits, covered in best NRE fixed deposit rates and how they work.

But — and this is crucial — the long-run drift is gentle and the short-run noise is large. In any given month, the rupee can move either way by more than its average annual drift. So the long-run trend tells you something about decade-scale savings decisions and almost nothing about whether to send money this Tuesday or next. Don't confuse the two timescales.

How to actually watch the rupee (if you must)

If you're going to keep an eye on USD/INR, watch the drivers, not the rate itself — the rate is the output; the drivers are where the story is. A short watchlist that tells you more than the daily quote:

Brent crude prices. The most direct lever for the rupee. A sustained climb in oil is a headwind for the currency; falling oil is a tailwind. If you only track one thing, track this.

The US Federal Reserve's direction. When the Fed is raising rates or signaling "higher for longer," the dollar tends to strengthen and emerging-market currencies like the rupee feel pressure. When the Fed pivots toward cuts, that pressure can ease.

Foreign investor flows into Indian markets. Reported regularly in the financial press as FII/FPI inflows and outflows. Sustained outflows signal rupee pressure; strong inflows support it.

The broad dollar index (DXY). This tells you whether a rupee move is really about India or just about a globally strong dollar dragging everything down. A rising DXY with a falling rupee usually means "strong dollar," not "weak India."

None of these let you predict next week. What they do is let you understand what's happening and why, so you're never blindsided by a move and never fooled into thinking a global dollar story is an India story.

The real exchange rate vs the one you see

One concept worth knowing, because it reframes the "rupee always falls" worry: economists track something called the real effective exchange rate, which adjusts the headline rate for inflation differences between countries. The rupee's gradual slide against the dollar in nominal terms is, to a large degree, just the arithmetic of India running higher inflation than the US over time. In real terms — adjusted for that inflation gap — the rupee has been far more stable than the scary-looking nominal chart suggests.

Why does this matter to you? Because it means the long, slow nominal decline isn't a sign of crisis or mismanagement; it's largely the expected consequence of an inflation differential. For an NRI, it's a reminder to judge Indian rupee returns — like a tax-free deposit yielding 7% — against the likely nominal drift of the rupee, not to panic about the currency as if it were collapsing. The slide is gradual, structural, and mostly predictable in direction if not in timing.

What this means for your transfers

If forecasting is unreliable, what do you do with all this? A few sensible things.

Treat the forces as context, not signals. Knowing oil is spiking helps you understand why your rate got worse; it does not reliably tell you to wait, because the market has already priced the oil move in. The same goes for every driver above — by the time you've read the headline, the rate reflects it.

For regular transfers, ignore the forecasts entirely and convert on a schedule, letting the averaging smooth out the noise. For large or time-sensitive transfers, don't bet on a direction — remove the risk by locking a rate. Both strategies are laid out in best time to convert USD to INR and forward contracts and rate locks for NRIs.

And keep the cost you can control in focus. You'll lose far more, far more reliably, to a bad provider's rate margin than to any short-term swing in the rupee. Getting your transfer service right, per best ways to send money from USA to India, beats every forecast.

A note on reading forecasts wisely

You'll keep seeing rupee forecasts, and they're not useless — a range from a serious institution, with the reasoning attached, tells you what professionals think the balance of forces points toward. That's worth knowing. What's not worth trusting is a single precise number presented as fact, or a forecast with no reasoning. When you read one, ask: what does it assume about oil, US rates, and global risk appetite? If those assumptions shift — and they will — the forecast shifts with them. Treat forecasts as conditional scenarios, not predictions, and you'll use them the way the professionals who write them actually intend.

Turning understanding into action

Knowing the drivers is satisfying, but the point is better decisions. For everyday transfers, the honest application of all this is almost anticlimactic: don't act on it. Convert on a schedule and let averaging absorb the swings, as argued in best time to convert USD to INR. The drivers explain the weather; they don't tell you which afternoon to send your rent.

Where this knowledge genuinely pays off is on the big, infrequent transfers. If you're moving a large sum for a property purchase or relocating savings, a 2–3% rupee swing translates into real money, and understanding that oil, rate gaps, and dollar strength could push the rate against you is the case for removing the risk rather than betting on it — see large money transfers to India and forward contracts and rate locks for NRIs. And whatever the rate does, you'll still lose more to a bad provider's margin than to a market move, so getting the transfer mechanics right via the complete guide to sending money from the USA to India and confirming costs with how much INR you'll receive after fees remains the highest-value thing you can do. Read the forces for context; act on the fundamentals you control.

Sources & further reading

- Reserve Bank of India — Foreign Exchange Reserves & Intervention Data

- U.S. Federal Reserve — Federal Open Market Committee (FOMC) policy and rate decisions

- U.S. Energy Information Administration — Brent Crude Oil Spot Prices

- National Securities Depository Limited (NSDL) — FPI/FII Investment Flows

- Federal Reserve — Nominal Broad U.S. Dollar Index (DXY proxy, DTWEXBGS)

Frequently asked questions

Will the rupee get stronger or weaker? No one can reliably say in the short term. Over the long run the rupee has trended gradually weaker against the dollar, driven by higher relative inflation and oil imports. Short-term direction depends on oil prices, US–India rate gaps, foreign investment flows, and global dollar strength, which shift unpredictably.

What makes the rupee fall? Rising crude oil prices (India imports most of its oil and pays in dollars), high US interest rates relative to India, foreign investors pulling money out of Indian markets, and broad strength in the US dollar during global stress. These often combine, and the RBI then steps in to slow — not reverse — the move.

How does oil affect the rupee? India imports the majority of its oil and pays in dollars, so higher oil prices mean buying more dollars (selling more rupees), which weakens the currency. Oil is one of the most direct and watchable drivers of USD/INR for this reason.

Does the RBI control the exchange rate? The RBI manages the speed of currency moves, not the direction. It uses its foreign-exchange reserves to smooth sharp swings and prevent panic, but it generally won't reverse a move driven by fundamentals, since doing so would drain reserves quickly.

General information, not financial advice or a forecast. Currency markets are unpredictable; nothing here guarantees future rates. Confirm current data before making decisions.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.