Complete Guide to Sending Money from the USA to India

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

India receives more money from its diaspora than any other country on earth — well over a hundred billion dollars a year flows home from Indians living abroad, and a large slice of it starts in the United States. Behind that staggering number are millions of ordinary, repeated decisions: a daughter in Texas sending rent to her parents, an engineer in California building savings back home, a son covering a medical bill in a hurry. If you're one of them, this is the one article meant to orient you on all of it — what to choose, how not to overpay, and what to watch as the amounts get bigger.

Think of this as the map. Each section points to a deeper article when you want detail, but on its own it'll get you sending money sensibly and cheaply.

Start with the one thing that decides cost

Before choosing any service, internalize a single idea, because it governs everything else: the cost of a transfer is the fee plus the exchange rate markup, and the markup is usually the bigger, hidden part.

The rate you see on Google — the mid-market rate — is almost never the rate you actually get. Services shave a margin off it and keep the difference, and that margin is often larger than any visible fee. A service can advertise "zero fees" and still cost you more than one charging a small fee, because it buried the cost in a worse rate. So the only honest way to compare two services is to look at the rupees that actually land in India for your exact amount. That number captures everything. We unpack the math in how much INR you'll receive after fees and the hiding places in hidden fees in USD to INR transfers. If you remember nothing else, remember to compare delivered rupees, not fees.

Choosing how to send

There are essentially four routes, and they suit different needs.

Transfer apps — Wise, Remitly, Xoom, Instarem, and others — are the default winner for most personal transfers. They give rates close to the real market rate, charge transparent fees, and deliver to an Indian bank account in minutes to a couple of days. They avoid the costly correspondent-bank chain that makes wires expensive. For ordinary monthly support to family, one of these is almost certainly your answer. The three biggest are compared head-to-head in Wise vs Remitly vs Xoom.

Bank wires feel safe and are usually the most expensive option for ordinary amounts, because the bank marks down the rate and routes your money through intermediary banks that each take a cut. The "safety" is mostly familiarity — apps are licensed and regulated too. The full case is in why banks give worse exchange rates than remittance apps. Wires earn their place mainly on very large, negotiated transfers.

Retail money transfer operators like Western Union and Ria shine when your recipient needs cash pickup or lives somewhere apps don't reach well. You pay for that reach through a wider margin, but for cash in hand in a small town, they deliver.

Indian banks' own remittance services (like ICICI Money2India or SBI's remittance arm) are convenient when you're sending to your own NRE/NRO account, since they're built for exactly that flow.

The full breakdown of which route fits which situation is in best ways to send money from USA to India.

Sending to family vs sending to yourself

A distinction worth drawing early, because it changes the playbook.

If you're sending to family — parents, a sibling, a spouse — you're depositing into their ordinary Indian bank account, and your main concerns are cost, speed, and getting the details right. Straightforward.

If you're sending to yourself — building savings, parking money in India, preparing to move back — you'll be sending into an NRE or NRO account, and which one matters a lot. An NRE account holds foreign earnings you bring in, with tax-free interest and full freedom to take the money back out. An NRO account holds income you earn within India, like rent or dividends, and it's taxed with a yearly limit on moving money out. Picking the wrong one creates tax and repatriation headaches. The full logic is in NRE vs NRO accounts explained.

How the delivery method changes things

Once you pick a service, you often choose how the money lands. The main options into India:

Bank deposit is the standard — money goes straight into the recipient's account, cheap and reliable, typically a few minutes to a couple of days. UPI is increasingly supported and very fast for smaller amounts. Cash pickup lets the recipient collect physical cash at a branch or agent location, useful when they lack a bank account or need cash now, but usually pricier. Wallet or debit-card deposit exists with some services for speed.

The trade-offs — speed vs cost vs convenience — are laid out in cash pickup vs bank deposit. For most family transfers, a bank deposit funded from your US checking account is the sweet spot.

Funding: the choice that quietly changes your cost

How you pay for the transfer matters as much as which service you use. Funding from your bank account (ACH) is almost always the cheapest method, though it takes a day or two longer. Funding with a debit or credit card is faster but costs more, and a credit card may trigger a cash-advance fee plus immediate interest from your card issuer — a cost outside the transfer service entirely. The rule: bank-funded and patient beats card-funded and fast, on cost. Reserve card funding for genuine emergencies.

Timing: do less than you think

The instinct to wait for a "better" rate burns more people than it helps. Short-term rupee moves are genuinely unpredictable, and the forces behind them — oil prices, US–India interest rate gaps, foreign investment flows, the RBI — are already priced into the rate by the time you read the news. We cover those drivers in USD to INR forecast and key drivers.

For regular transfers, the winning approach isn't timing — it's converting a steady amount on a schedule, which averages out the noise and stops you from waiting yourself into a worse rate or a missed payment. For large, one-off transfers, don't guess the direction; consider locking the rate instead. Both ideas live in best time to convert USD to INR and forward contracts and rate locks for NRIs.

Limits, taxes, and reporting

For ordinary amounts, none of this will trouble you. As the sums grow, a few things come into view.

There's no single legal cap on sending personal money from the US to India, but each service sets its own limits that rise with identity verification. Large gifts can involve US reporting: gifting more than the annual exclusion ($19,000 in 2026) to one person means filing IRS Form 709, though you almost never owe actual tax, since it draws on a multi-million-dollar lifetime exemption. Receiving more than $100,000 from a foreign person triggers Form 3520, a reporting form with real penalties for skipping it. And any transfer over $10,000 is auto-reported by the bank — routine, nothing to do on your end.

On the India side, gifts from close relatives are generally tax-free for the recipient regardless of size, so your parents receiving your support typically owe no Indian tax. The detail is in NRI tax rules on money sent to India, large money transfers to India, and FBAR and Form 3520 for the account-reporting side.

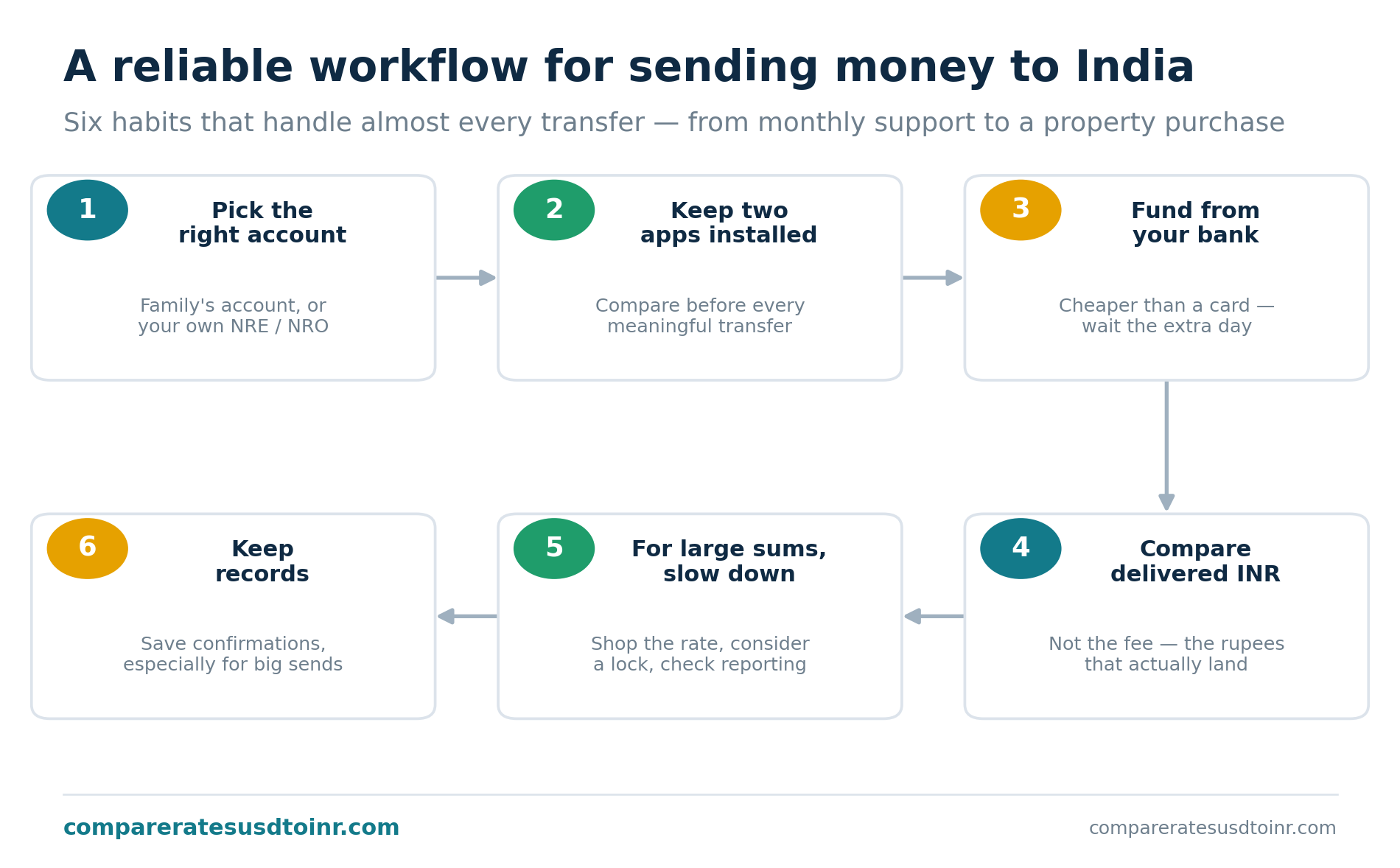

A simple, reliable workflow

Pulling it together, here's a routine that handles almost every case well:

| Step | What to do |

|---|---|

| 1. Pick a recipient account | Family's bank account, or your own NRE/NRO — get the account type right |

| 2. Keep two apps installed | Compare delivered rupees before each meaningful transfer |

| 3. Fund from your bank | Cheaper than card; wait the extra day if you can |

| 4. Compare delivered INR | Not fees — the rupees that land decide the winner |

| 5. For large sums, slow down | Shop the rate hard, consider a rate lock, check reporting |

| 6. Keep records | Save confirmations, especially for large or recurring transfers |

For regular support, automate it but revisit the rate occasionally — see recurring transfers to India. For a property purchase, read the property-specific guide first, since account choice and resale repatriation have their own rules: sending money to India for property purchase.

The traps to sidestep

A handful of mistakes account for most of the money people lose. Trusting a "no fee" banner without checking the rate. Funding with a credit card and eating a cash-advance fee. Picking a long-term provider based on a one-time promotional rate that later expires. Waiting for a better rate until a bill goes overdue and converting in a panic. Sending a wire when an app would have delivered more rupees. And, on the careless end, fat-fingering an account number — always double-check recipient details, and never send money to someone pressuring you with urgency, which is the signature of a scam.

Avoid those six and you're already ahead of most senders.

Find your situation

Different senders need different things, so here's a quick way to locate yourself and skip to what matters.

| If you're... | Your main concern | Start here |

|---|---|---|

| Sending monthly support to parents | Low cost, set-and-forget | Best ways to send money; recurring transfers |

| Building savings in India | Right account type, currency risk | NRE vs NRO; best NRE FD rates |

| Making a one-time large transfer | Rate margin, reporting, timing risk | Large money transfers; forward contracts |

| Buying property in India | Account choice, resale repatriation | Sending money for property |

| Suspicious you've overpaid | Finding the hidden markup | Hidden fees; markup vs fee |

| Just comparing apps | Which delivers the most rupees | Wise vs Remitly vs Xoom |

The point of mapping it out is that "sending money to India" isn't one task — it's half a dozen related ones, and the right move depends on which you're actually doing. A monthly $500 to family and a one-time $90,000 for a flat share almost nothing in common except the destination country.

A word on scams, because it matters most

The single most expensive mistake isn't a bad rate — it's sending money to the wrong person. Scams targeting the diaspora are common and clever: a "relative" in sudden trouble, a too-good investment, a romance that needs emergency funds, an official-sounding demand for immediate payment. The tell is almost always urgency combined with pressure to send right now to someone you can't fully verify. No legitimate situation requires you to wire money to a stranger within the hour. Slow down, verify independently through a channel you trust, and never let urgency override that check. A transfer you regret on a rate costs you a few thousand rupees; a transfer to a scammer can cost you everything you sent, with no recovery. Getting the recipient right is more important than getting the rate right.

Where to go next

If you're sending to family for the first time, start with best ways to send money from USA to India and Wise vs Remitly vs Xoom. If you're saving in India or planning to move back, read NRE vs NRO accounts explained. If you suspect you've been overpaying, hidden fees in USD to INR transfers will show you where it went. And if a large transfer is coming, large money transfers to India covers the limits, reporting, and rate risk that suddenly matter at scale.

Sending money home shouldn't be stressful or expensive. Get the service and funding right, compare delivered rupees, don't try to outguess the market, and slow down when the sums get large. That's the whole craft.

Sources & further reading

- IRS — About Form 709, U.S. Gift (and GST) Tax Return

- IRS — Large gifts or bequests from foreign persons (Form 3520)

- FinCEN — Report of Foreign Bank and Financial Accounts (FBAR)

- RBI — Master Direction: Deposits and Accounts (NRE/NRO/FCNR)

- Wise — Pricing & fees

Frequently asked questions

What is the best way to send money to India? For most personal transfers into a bank account, a transfer app (Wise, Remitly, Instarem) funded from your US bank account gives the best combination of low cost and good rates. Compare the delivered rupees across two services before sending — the winner shifts with promotions and funding methods.

Is sending money to India taxable? Sending isn't taxed by itself. Gifts to close relatives in India are generally tax-free for the recipient. On the US side, gifting above the annual exclusion ($19,000 in 2026) means filing Form 709, but you typically owe no tax. Large amounts may trigger reporting forms, not necessarily tax.

How long does a transfer to India take? From a few minutes to about three business days. Express options and cash pickup can be near-instant; cheaper bank-funded transfers take a day or two because the ACH pull from your US account is slower.

How much can I send to India? There's no single legal cap on personal transfers from the US to India. Limits come from your service (rising with verification) and from US gift-reporting thresholds on very large amounts. Moving money out of India is separately capped at USD 1 million per year from an NRO account.

General information, not tax, legal, or financial advice. Rates, fees, limits, and tax rules change — confirm current details with providers and a qualified professional before acting.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.