NRE vs NRO Accounts Explained for NRIs (2026 Guide)

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

Reviewed for accuracy against primary IRS, FinCEN, and RBI sources. General information, not personal tax or legal advice — confirm your own situation with a qualified professional.

The first time someone moves abroad and tries to keep their Indian bank account, a confusing thing happens: the bank tells them they can't. Once you become a non-resident under Indian law, your old resident savings account is no longer valid for you. You're supposed to convert it — and that's the moment you run into the alphabet soup of NRE and NRO accounts, usually with no idea which one you need.

The two look similar on a bank's website, and the names give nothing away. But they're built for opposite purposes, and choosing wrong can cost you in tax or lock up money you wanted to move. Once the logic clicks, it's actually simple. The whole distinction comes down to one question: where did the money come from?

The one idea that explains everything

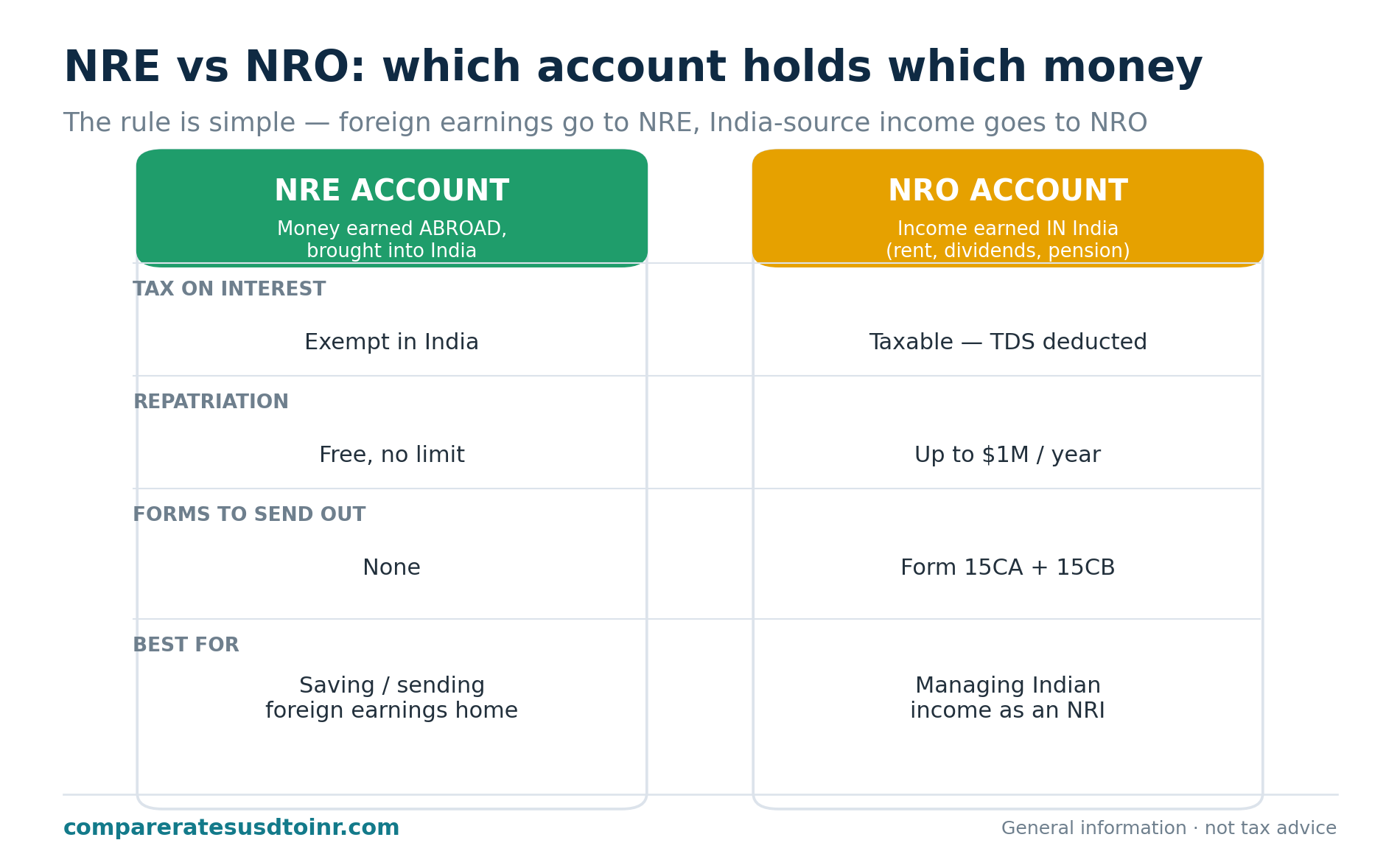

An NRE account (Non-Resident External) is for money you earn outside India and bring in. Your US salary, your savings in dollars, money you want to park in India from abroad — that goes into an NRE account. Because it's foreign-earned money, India treats it generously: the interest is tax-free in India, and you can take the money back out, in full, whenever you want.

An NRO account (Non-Resident Ordinary) is for money you earn inside India while living abroad. Rent from a flat you own in Bengaluru, dividends from Indian shares, a pension, interest from old deposits, proceeds you're managing for family — that's Indian-source income, and it belongs in an NRO account. Because it's income arising in India, India taxes it, and there are limits on how much you can move out per year.

That's the heart of it. NRE = foreign money coming in, tax-friendly, freely movable. NRO = Indian money you're holding while abroad, taxed, with a yearly export cap. Almost every other difference flows from this single distinction.

Side by side

| Feature | NRE Account | NRO Account |

|---|---|---|

| Source of funds | Income earned abroad (e.g., US salary) | Income earned in India (rent, dividends, pension) |

| Currency held | Indian rupees | Indian rupees |

| Tax on interest in India | Exempt | Taxable; TDS deducted (commonly ~30% plus surcharge/cess) |

| Repatriation (taking money out) | Freely repatriable, principal and interest, no cap | Up to USD 1 million per financial year, after tax compliance |

| Forms needed to repatriate | None | Form 15CA and 15CB (from a chartered accountant) |

| Exchange rate risk | Yes — funds sit in rupees | Yes — funds sit in rupees |

| Joint account with a resident | Allowed only on "former or survivor" basis | Allowed, can be held jointly with a resident |

| Who it suits | NRIs sending foreign earnings home or saving in India | NRIs with ongoing Indian income to manage |

The tax line is the one that surprises people most. On an NRE fixed deposit, the interest lands in your account untouched. On an NRO account, the bank deducts tax at source — often around 30% plus surcharge and cess — before you ever see the interest. If your country has a tax treaty with India (the US does), you may be able to lower that rate by filing a Tax Residency Certificate and Form 10F, but the default deduction is steep, and it catches people off guard.

So which one do you actually need?

For most NRIs in the US sending money home, the answer is an NRE account, and often that's the only one they need. You earn in dollars, you want to move savings to India, you'd like the interest tax-free, and you want the freedom to pull it all back if your plans change. NRE checks every box.

You need an NRO account when you have money coming from India. Bought a flat before you left and now rent it out? That rent has to go somewhere legitimate — an NRO account. Still hold Indian mutual funds or shares paying dividends? NRO. Receiving a pension from past Indian employment? NRO. The NRO account is essentially the compliant home for your Indian-source income while you're a non-resident.

Plenty of NRIs hold both, and that's normal — an NRE account for foreign earnings and savings, an NRO account for the Indian income stream. They're not competing; they're doing different jobs.

A real example makes it tangible. Priya, a software engineer in Seattle, sends part of her US salary home every month to build savings and support her parents — that flows into her NRE account, where it earns tax-free interest and stays fully repatriable if she ever moves back. She also inherited a small apartment in Chennai that she rents out for ₹25,000 a month. That rent can't go into the NRE account, because it's Indian income — it goes into her NRO account, where it's taxed, and from which she can repatriate up to a yearly limit if she chooses.

The repatriation difference, in practice

"Repatriation" just means moving money out of India, back to wherever you live. This is where NRE and NRO really diverge.

From an NRE account, repatriation is effortless. Principal and interest, no upper limit, no special forms, no approval. The money was foreign to begin with, so India lets it leave freely. If you might need access to these funds abroad, that flexibility is a genuine advantage.

From an NRO account, there's a ceiling: up to USD 1 million per financial year, and only after you've squared away the tax and produced two forms from a chartered accountant — Form 15CA and Form 15CB. It's manageable, and a million dollars a year covers almost everyone, but it's a process, not a button. We walk through it step by step in how to repatriate money from India to the USA.

The catch nobody mentions: currency risk

Here's something the tax-free headline can obscure. Both NRE and NRO accounts hold rupees. The moment you convert dollars into an NRE deposit, you're exposed to the rupee. If the rupee weakens against the dollar over the years — which has been the long-run trend — the dollar value of your tax-free rupee interest can shrink, sometimes by more than the interest gained.

That doesn't make NRE accounts a bad idea. For money you'll eventually spend in India, holding rupees is exactly right, and the tax-free interest is real. But for money you might bring back to the US, factor in that a 7% tax-free rupee return can be eroded if the rupee slides 3–4% against the dollar that year. We unpack this trade-off in best NRE fixed deposit rates and how they work, and the forces moving the rupee are covered in USD to INR forecast and key drivers.

Opening and converting: the practical steps

If you already had a resident savings account before moving abroad, you don't open fresh — you convert or re-designate it, and you're required to do so once your status changes to non-resident. Most banks let you do this remotely now, with attested copies of your passport, visa or work permit, proof of overseas address, and a fresh KYC. Many NRIs open NRE and NRO accounts as a linked pair with the same bank, which makes moving between them and managing both simpler.

When you're sending money from the US into your NRE account, the same transfer apps and bank remittance arms covered in best ways to send money from USA to India apply — you're just sending to your own account instead of a family member's. Watch the exchange rate the same way; a tax-free deposit funded at a bad conversion rate isn't the bargain it looks like.

Mistakes NRIs make with these accounts

A few errors come up again and again, and each is avoidable.

The first is not converting the old resident account at all. People move abroad, keep using their existing resident savings account out of habit, and don't realize that's no longer permitted once they're a non-resident. The fix is to convert it to NRO (or open NRE/NRO afresh) when your status changes. Continuing to run a resident account as a non-resident is a compliance problem waiting to surface.

The second is routing Indian income into an NRE account. Rent or dividends are Indian-source money, and they belong in an NRO account. Pushing them into an NRE account to chase the tax-free treatment isn't allowed and can unravel messily later. Keep foreign money in NRE and Indian money in NRO — the wall between them exists for a reason.

The third is forgetting about the TDS on NRO interest. The bank deducts tax at source on NRO interest at a steep rate, and people are startled when their interest shows up smaller than expected. If your country has a tax treaty with India, file a Tax Residency Certificate and Form 10F to bring that rate down — but you have to actually submit the paperwork; it isn't automatic.

The fourth is ignoring what happens when you move back to India. When you return for good and become a resident again, your NRE and NRO accounts must be re-designated to resident accounts. NRE funds can often be moved into an RFC (Resident Foreign Currency) account if you want to keep holding foreign currency. Sorting this out promptly on return keeps you on the right side of the rules and preserves your options.

A quick decision guide

If you're earning abroad and want to save in India, support family, or keep flexible access to your money: open an NRE account. If you have rent, dividends, a pension, or any income arising within India that you need to hold and manage as a non-resident: open an NRO account. If you have both kinds of money — which many NRIs do — open both, and keep each type of income in its correct account. Mixing them isn't just untidy; it can create tax and compliance headaches you'd rather avoid.

Where this fits in your bigger plan

The account choice is the foundation, but it connects to everything else about moving money home. Once your NRE account is open, funding it well matters — sending dollars into it at a poor exchange rate quietly erodes the tax-free benefit you opened it for, so apply the same delivered-rupees comparison you'd use for any transfer, covered in the complete guide to sending money from the USA to India and best ways to send money from USA to India.

If you're funneling a large sum into an NRE account — say, savings you're moving home or money for a property — the limits, reporting, and rate-risk considerations in large money transfers to India come into play, and buying property has its own account and repatriation wrinkles worth reading first. When the time comes to move money the other way, the NRE vs NRO distinction directly shapes how easily you can do it: NRE funds flow out freely, NRO funds hit the yearly cap and the two CA forms. That whole process is in how to repatriate money from India to the USA. And if you're parking money in NRE fixed deposits for the tax-free interest, weigh that against rupee depreciation using best NRE fixed deposit rates and the drivers in USD to INR forecast and key drivers.

Sources & further reading

- Reserve Bank of India — FAQs on Accounts in India by Non-Residents (NRE/NRO/FCNR)

- RBI Master Direction — Deposits and Accounts (NRE/NRO/FCNR account rules)

- Income Tax Department (India) — Form 15CA/15CB e-filing for foreign remittances

- IRS — Foreign Tax Credit (relief for tax paid to India under the US-India treaty)

- IRS — Report of Foreign Bank and Financial Accounts (FBAR) for NRE/NRO accounts

Frequently asked questions

Is NRE or NRO better for NRIs? Neither is "better" outright — they serve different money. Use NRE for foreign earnings you bring into India (tax-free interest, full repatriation) and NRO for income that arises in India like rent or dividends (taxable, with a yearly repatriation cap). Many NRIs need both.

Is interest on an NRE account taxable? Interest on an NRE account is exempt from Indian income tax as long as you hold non-resident status, and banks don't deduct TDS on it. NRO interest, by contrast, is taxable and subject to TDS.

Can I repatriate money from an NRO account? Yes, up to USD 1 million per financial year, after meeting tax obligations and submitting Form 15CA and Form 15CB from a chartered accountant. NRE funds, by contrast, are freely repatriable with no cap.

Can a resident be a joint holder on an NRE account? An NRE account can be held jointly with a resident relative only on a "former or survivor" basis. NRO accounts allow more flexible joint holding with residents. Check your bank's current policy, as rules are periodically updated.

This is general educational information, not tax or financial advice. Tax rates, TDS, and repatriation rules change — confirm current details with your bank or a qualified chartered accountant before acting.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.