Best Time to Convert USD to INR: What Works in 2026

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

Every NRI I know has, at some point, sat on a transfer waiting for the rupee to "get better." Sometimes it works out. More often, three weeks later the rate is worse, the bill they were waiting to pay is now overdue, and they convert anyway at a number they'd have been thrilled to take earlier. The urge to time the market is universal. The results are humbling.

So let me be straight before getting into the nuance: you almost certainly cannot predict where the rupee is going, and neither can the banks that employ rooms full of analysts to try. But that doesn't mean timing is pointless. There's a difference between forecasting the rupee — a fool's errand — and not actively sabotaging yourself on timing, which is very doable. The second one is where the real, modest gains live.

Why you can't time the big moves

The USD/INR rate is pushed around by forces no individual sender can see coming: crude oil prices, the gap between US and Indian interest rates, foreign investors moving money in and out of Indian markets, and the Reserve Bank of India stepping in to smooth things out. These interact in ways that surprise professionals routinely. When someone tells you the rupee "will definitely hit X by December," they're guessing, however confident they sound.

The deeper problem is that the current rate already reflects everything the market collectively knows. If everyone expected the rupee to fall next month, it would mostly fall today, as people sold ahead of it. So waiting for an obvious, predictable drop is waiting for something the market has usually already priced in. The forces themselves are worth understanding — we cover them in USD to INR forecast and key drivers — but understanding them is not the same as being able to profit from short-term bets.

What actually moves the needle for you

Here's the reframe that helps. For most senders, the size of the cost you control through fees and rate margins is bigger and more reliable than the cost you're trying to control through timing. You might agonize over a 0.5% move in the rupee while routinely losing 2% to a bad provider's markup. Fix the second thing first. Picking a good service, as covered in best ways to send money from USA to India, will save you more, more dependably, than any timing strategy.

Once your provider is sorted, a few genuine timing habits help at the margins.

Send during market hours. Currency markets are most liquid, and spreads tightest, during overlapping US and European/Indian trading hours on weekdays. Some services widen their margin on weekends and holidays to protect against the rate moving while markets are shut. Converting Tuesday morning rather than Saturday night can shave a little off the spread, for free. Small, but real, and entirely within your control.

Avoid converting in a panic. The worst rates people accept are almost always under time pressure — a bill due today, an emergency, a deadline. When you're forced to convert now, you take whatever's offered. The fix isn't timing the market; it's not letting yourself get cornered. Which leads to the single most useful idea here.

The strategy that actually beats timing: don't try

For recurring transfers — monthly support to family, regular savings home — the winning move isn't to time anything. It's to convert a consistent amount on a regular schedule, regardless of the rate. This is dollar-cost averaging, and it's not exciting, which is exactly why it works.

By converting, say, $1,000 on the same date every month, you automatically buy more rupees when the rupee is weak and fewer when it's strong. Over a year, you land near the average rate, and you completely sidestep the emotional trap of waiting for a "good" rate that may never come. You stop checking the chart anxiously. You stop missing payments while you wait. You stop converting in a panic at bad rates. The average sender who does this beats the average sender who tries to time, not because the strategy is clever, but because it removes the mistakes. We get into the mechanics in recurring transfers to India.

If a chunk of your transfer is discretionary — savings you don't urgently need to move — you can still split it: convert part on schedule, and keep a portion flexible to send if the rupee happens to weaken sharply. But treat that flexible portion as a small bonus opportunity, not the main plan.

When timing genuinely matters: large, one-off sums

The calculus changes for a big, single transfer — a property down payment, moving years of savings home, a major family obligation. On $80,000, a 2% swing in the rupee is ₹1,40,000 or so. That's real money, and "just convert on a schedule" doesn't apply to a one-time event.

For these, the answer usually isn't to guess the direction. It's to remove the guessing. A forward contract or a rate lock lets you fix today's rate for a transfer you'll make later, so a sudden adverse move can't hurt you. You give up the chance of a better rate in exchange for certainty, which is often the right trade when the sum is large and the timeline matters. We explain how these work, and when they're worth it, in forward contracts and rate locks for NRIs.

If you can't or don't want to lock a rate, the next-best approach for a large sum is to break it into a few transfers over a few weeks rather than converting everything at one moment. That doesn't improve your average — it just protects you from the bad luck of converting the entire amount on the single worst day. It's insurance against regret, not a way to win.

Dollar-cost averaging, with actual numbers

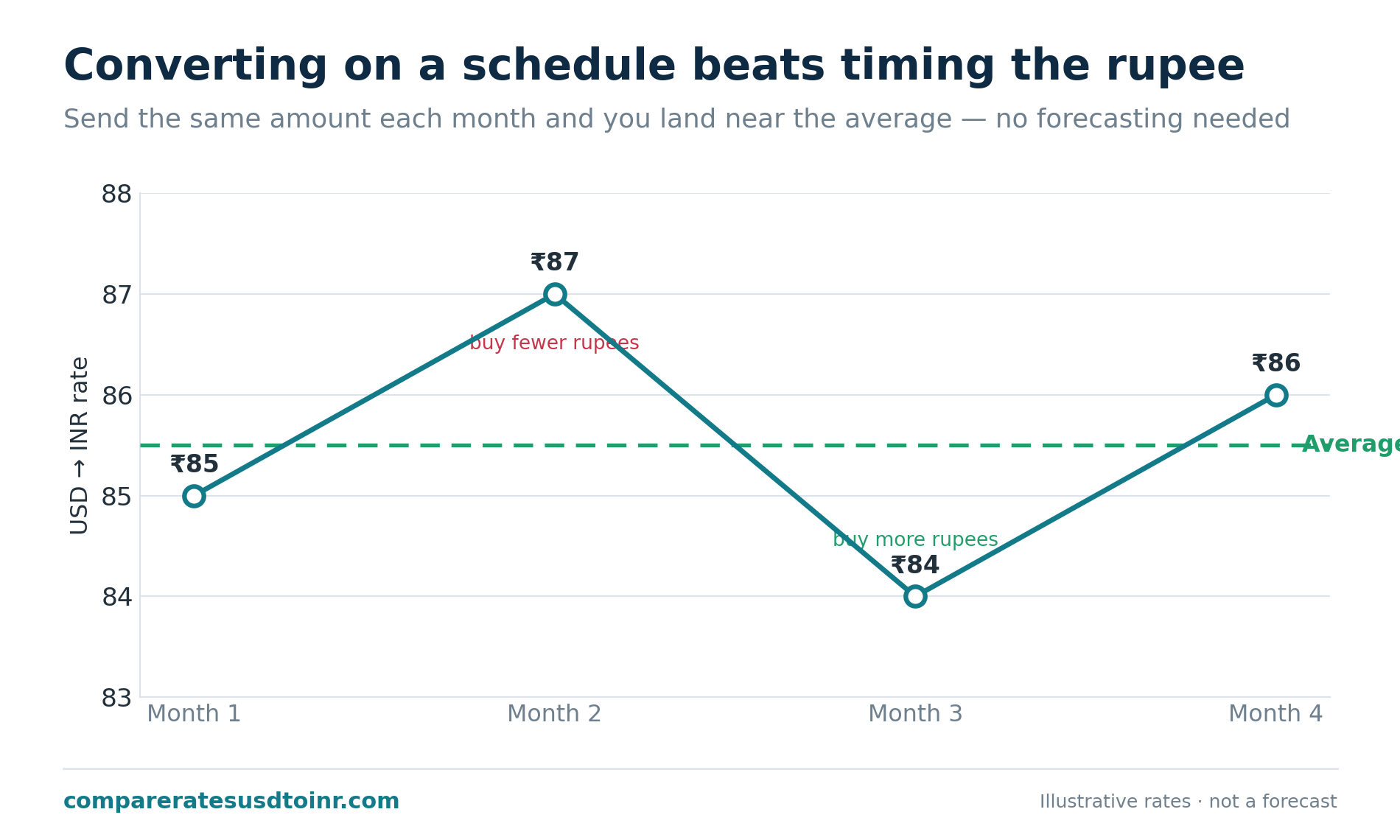

The case for converting on a schedule is easier to believe when you see it play out. Imagine you convert $1,000 every month for four months, and the rupee bounces around: ₹85 in month one, ₹87 in month two, ₹84 in month three, ₹86 in month four.

Convert mechanically each month and you buy ₹85,000, then ₹87,000, then ₹84,000, then ₹86,000 — a total of ₹3,42,000 for your $4,000, which works out to an average of ₹85.50 per dollar. You didn't have to predict anything. You automatically bought a few more rupees in the cheap month (the ₹84 one bought you the most) and a few fewer in the expensive month, and you landed right at the average.

Now picture the alternative: you tried to time it. You waited in month one because ₹85 felt low, waited again in month two as it climbed to ₹87 hoping it would fall, panicked in month three when a bill came due and converted everything at... whatever the rate happened to be that day. The timer almost always ends up worse than the averager, not because the strategy is dumb, but because human emotion under uncertainty makes poor calls. Averaging works precisely because it takes the decision — and the emotion — out of your hands.

The psychology that costs people money

It helps to name the trap directly. The pain of converting at ₹85 and watching the rupee weaken to ₹86 the next week feels much sharper than the equal-and-opposite pleasure of converting at ₹86 and watching it strengthen. That asymmetry — losses hurting more than equivalent gains feel good — pushes people to wait, hoping to avoid the regret. But waiting just trades one regret for another, and adds the risk of being forced to convert under deadline pressure.

Recognizing this is half the cure. You're not actually trying to win the currency game; you're trying to stop your own instincts from making you lose it. A schedule, a rate lock for big sums, and a refusal to let yourself get cornered by a deadline — those three habits beat the cleverest market view, because they remove the moments where the bad decisions get made.

The patterns people swear by (and what to make of them)

You'll hear confident claims: the rupee weakens at fiscal year-end, it dips around oil-price spikes, it moves after RBI policy meetings, it's worse late in the calendar year. Some of these have a grain of truth — oil prices really do pressure the rupee because India imports most of its crude, and the rupee really has trended weaker against the dollar over the long run.

But here's the catch with all of them: even when a pattern is real, it's not reliably tradeable. The market knows about year-end flows too, and prices them in. The long-run weakening trend is gentle and noisy enough that any given month can go either way. Treating these patterns as actionable signals leads right back to the waiting game that burns people. Useful as background context, dangerous as a basis for sitting on a transfer you need to make.

A sane approach, summarized

Don't try to forecast the rupee — you'll lose more to the attempt than you'd ever gain. Get your provider and funding method right first, because that saves more than timing ever will. For regular transfers, convert a steady amount on a schedule and stop watching the chart. For a large one-off, consider locking the rate or splitting the conversion across a few dates to avoid a single bad moment. Send during weekday market hours when you can. And above all, don't let yourself get forced into converting under deadline pressure, because that's where the genuinely bad rates get accepted.

The unglamorous truth is that the people who do best with USD/INR aren't the ones with the sharpest market views. They're the ones who built habits that keep them from making mistakes. For the forces behind the rate, see USD to INR forecast and key drivers; for the rate-locking tools, forward contracts and rate locks.

How timing fits the rest of the picture

Timing is one lever, and not the biggest one. Before worrying about when to convert, make sure you've handled how — the provider and funding choices in the complete guide to sending money from the USA to India and best ways to send money from USA to India typically save more, more reliably, than any timing strategy. A 2% rate margin from a bad provider dwarfs the 0.5% you might gain from clever timing, and it's far easier to control.

If you're sending large or one-off amounts where timing genuinely matters, pair this with large money transfers to India, which covers the limits and reporting that come with size, and confirm you're not losing the saved money back to a hidden markup using how much INR you'll receive after fees. Timed well but converted through an expensive service, you've gained nothing — the two have to work together.

One last reframe to carry with you: the goal was never to beat the market. It was to stop the market from beating you through panic, deadline pressure, and waiting games. Get the provider right, convert regularly, lock big sums, and send during the trading week — do that and you've captured essentially all the timing benefit a normal person can realistically get.

Sources & further reading

- Reserve Bank of India — Foreign Exchange Rates and FEMA

- RBI — Reference Rate Archive (USD/INR daily reference rates)

- Investopedia — Dollar-Cost Averaging (DCA)

- Investopedia — Forward Contract

- IRS — Foreign Currency and Currency Exchange Rates

Frequently asked questions

Should I wait for a better USD to INR rate? Usually not. Short-term rate moves are unpredictable, and waiting often costs more than it saves — especially if you end up converting in a rush at a worse rate. For regular transfers, converting a steady amount on a schedule beats waiting. For large one-offs, consider locking the rate rather than guessing.

What time of day is best to transfer money to India? Weekday hours when major currency markets overlap and are most liquid tend to have the tightest spreads. Some services widen their margin on weekends and holidays, so converting during the trading week can shave a little off the cost.

Does the rupee fall at year end? There are seasonal flow patterns people point to, but they're not reliably tradeable — the market anticipates them. The rupee has weakened against the dollar over the long run, but any individual month is noisy. Don't sit on a needed transfer based on a calendar pattern.

Can I lock in an exchange rate? Yes. Forward contracts and rate-lock features let you fix today's rate for a transfer you'll complete later, which is useful for large or scheduled future transfers. You trade away potential upside for certainty. See our guide to forward contracts and rate locks for details.

General information, not financial advice. Currency markets are unpredictable; nothing here forecasts future rates. Confirm current rates and tools with your provider.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.