How to Compare Money Transfer Rates to India (USD → INR)

Send the same $1,000 to India through three different apps on the same afternoon and three different amounts of rupees land in the account. That is not a glitch — it is the whole reason comparing rates matters. The trick is knowing what to compare, because the number every provider puts in big font is rarely the number that decides how much your family actually receives.

This is a short, practical method for comparing USD → INR money transfer rates to India so you pick the best deal every time.

The two costs that decide how much arrives

Every transfer has two costs, and most people only look at one:

- The transfer fee — the upfront, visible charge ($0–$5, or a percentage). Easy to see, easy to compare.

- The exchange-rate margin — the gap between the real mid-market rate (what you see on Google or Reuters) and the rate the provider gives you. The provider keeps the difference. This is the hidden cost, and it is usually bigger than the fee.

A service can advertise "zero fees" and still be the most expensive option, simply by widening the margin. So a "$0 fee" banner tells you almost nothing on its own.

Compare on rupees received, not the headline rate

Because the fee is visible and the margin is hidden, the only fair way to compare money transfer rates to India is to ignore both in isolation and look at the bottom line:

How many rupees actually reach the recipient after the fee and the margin.

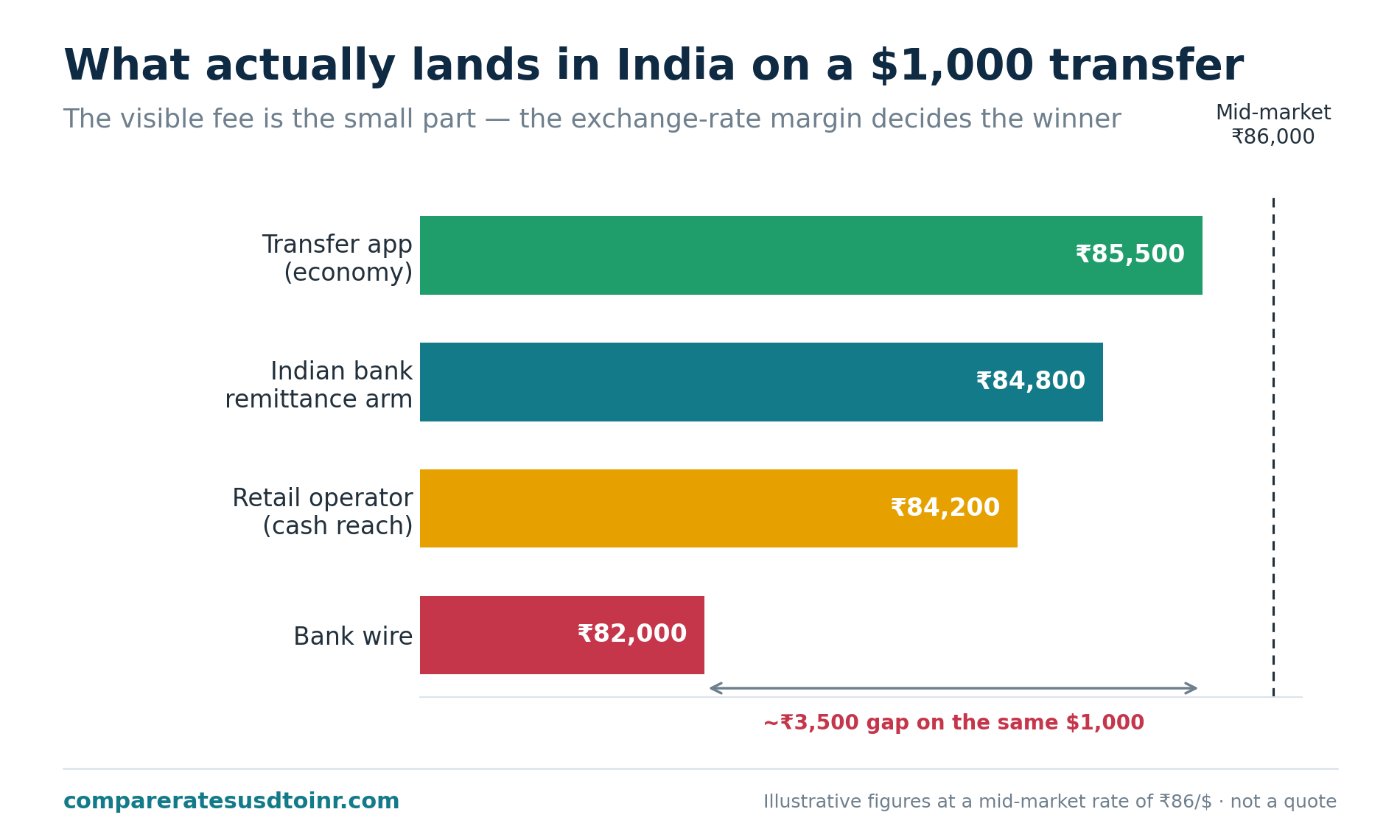

That single figure rolls up everything. A worked example on $1,000, with a true mid-market rate of ₹86.00 (so a perfect transfer would deliver ₹86,000):

| Provider | Advertised | Rupees delivered |

|---|---|---|

| A | "₹85.90, zero fees" | ₹85,900 |

| B | "₹85.50, zero fees" | ₹85,500 |

| C | "₹85.95, $5 fee" | ~₹85,520 |

All three shout "low/no fees," yet Provider A delivers ₹400 more than B on a single transfer. Over a year of monthly sends that is real money — and it is invisible unless you compare the delivered rupees.

A 60-second way to compare USD → INR transfer rates

- Open a live comparison such as our USD → INR rates table and enter the amount you actually plan to send.

- Sort by rupees received (not the exchange rate, not the fee).

- Note the top one or two — and check the gap to the rest, so you know how much a worse choice would cost you.

- Re-confirm the live quote on the winning provider's own site before you send; rates move through the day.

That is it. The provider with the highest delivered rupees for your amount is the best deal — full stop.

What actually changes the rate you get

The "best" provider is not fixed. It shifts with:

- The amount. On small sends a flat fee hurts proportionally more, so a fee-free option can win even with a slightly worse rate. On large sends the margin dominates and a tight, transparent rate pulls ahead. The crossover sits in the low thousands of dollars — so always compare at the amount you are actually sending.

- How you pay. Bank/ACH funding is cheapest; debit and especially credit cards add fees (and a card can trigger a cash-advance charge). A "cheap" service can become the expensive one the moment you pay by card.

- How it is delivered. Bank deposit, UPI, and cash pickup have different fees and timelines in India.

- Promotions. A great first-transfer bonus can flip the ranking once — but weigh the ongoing rate if you will send regularly.

- Timing. The underlying USD/INR rate moves daily; see best time to convert USD to INR for what actually helps.

Common mistakes when comparing

- Comparing the exchange rate alone. It ignores the fee.

- Trusting "zero fee." It can hide a wide margin — see hidden fees in USD to INR transfers.

- Comparing at the wrong amount. The winner changes with size — the maths is in how much INR you'll receive after fees.

- Assuming your bank is fine. Banks often apply the widest margins; why banks give worse exchange rates explains why.

- Picking once and never re-checking. The best provider for last month's transfer may not win this month's.

How our comparison works

Our live table aggregates USD → INR rates from major remittance providers, normalises every one to the same figure — rupees received after fees and margin — and ranks them from best to worst. We never hand-edit the order. Rates are indicative and refresh roughly every ten minutes; the provider's own checkout is always the final word.

For a head-to-head of the most popular apps, see Wise vs Remitly vs Xoom; for the full landscape, the best ways to send money from the USA to India.

Frequently asked questions

What's the best way to compare money transfer rates to India? Compare the rupees actually delivered after both the transfer fee and the exchange-rate margin, for the exact amount you plan to send — not the advertised exchange rate or the fee on their own. A live tool that ranks providers by delivered rupees does this for you in seconds.

What is the USD to INR transfer rate today? It changes constantly and differs by provider, because each adds its own margin to the mid-market rate. Check a live comparison for today's rates and, crucially, compare the rupees received rather than the headline number.

Does the cheapest service really change with the amount? Yes. On small transfers a fee matters most, so fee-free options often win; on large transfers the exchange-rate margin dominates, so the tightest rate wins. Always compare at the amount you are sending.

Is the headline exchange rate the real cost of sending money to India? No. The real cost is the mid-market rate minus what you receive, plus any fee. Two providers with similar headline rates can deliver very different rupees once the hidden margin is counted.

Figures here are illustrative and change daily. This is general information, not financial advice — confirm the live quote on the provider's own site before transferring.