Hidden Fees in USD to INR Transfers and How to Spot Them

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

A friend once forwarded me a screenshot, fuming. He'd sent $2,000 to his brother in Hyderabad through a service advertising "₹0 fees," felt smart about it, and then his brother reported receiving about ₹3,400 less than my friend had calculated using the rate from Google. "Where did it go?" he asked. "They said no fees."

They were telling the truth, technically. There was no fee. The money disappeared into the exchange rate instead — a place most people never think to look. This is the central trick of international transfers: the fee you can see is often the smallest cost, and the real money leaks out where you're not watching. Once you know the handful of places it hides, you can never be fooled again.

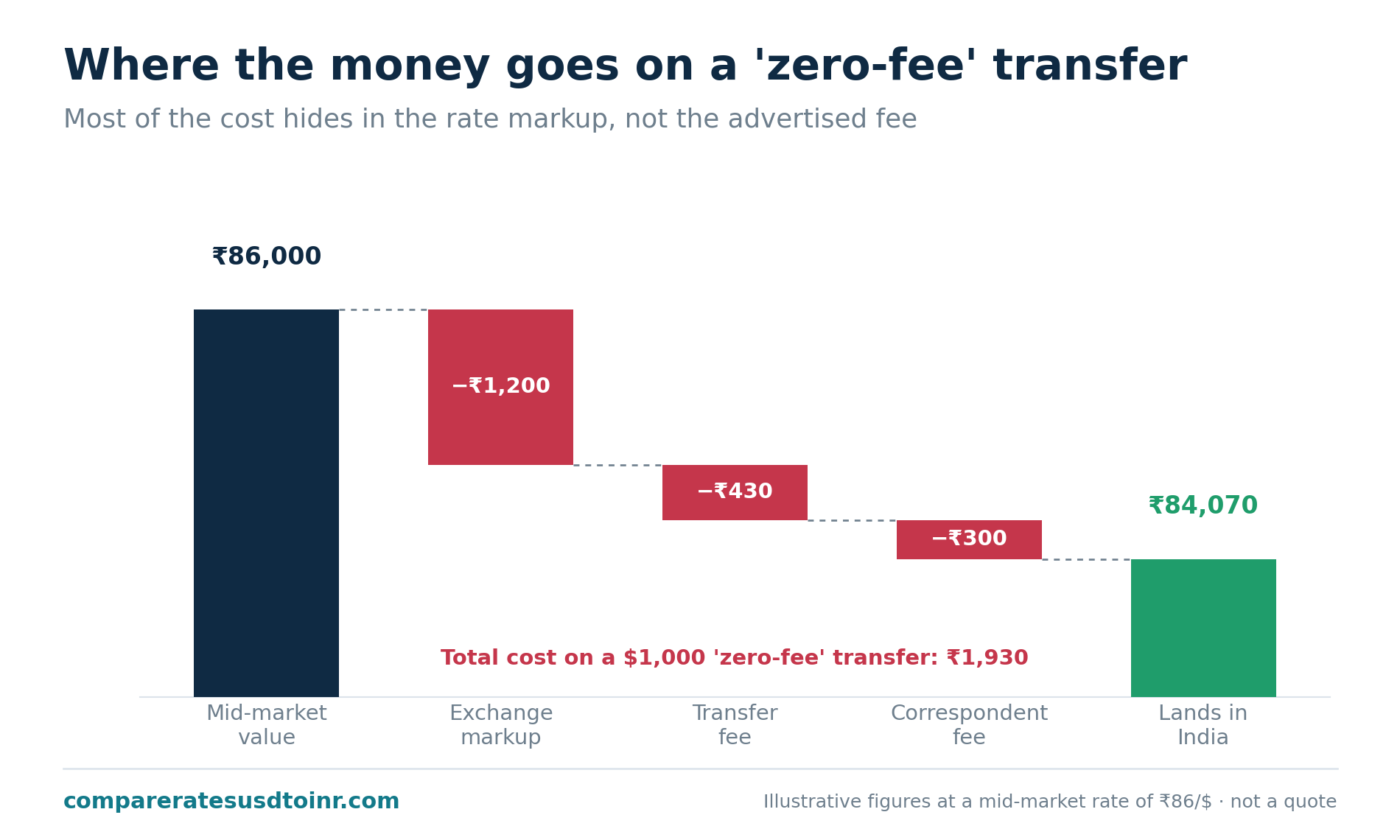

The big one: the exchange rate markup

Start here, because this is where most of the money goes. There's a "real" exchange rate — the mid-market rate, the midpoint of what the currency markets are actually trading at, the number Google shows you. Almost no consumer service gives you that exact rate. They give you a slightly worse one and keep the difference.

Say the mid-market rate is ₹86.00 to the dollar. A service might quote you ₹84.60. That ₹1.40 gap doesn't look like a fee — it just looks like "the rate" — but on $2,000 it's roughly ₹2,800 the service pocketed without ever charging you a cent in fees. That's the markup, sometimes called the FX margin or spread, and it's the single most expensive and least visible cost in the whole transfer.

The maddening part is how easy it is to hide. A company can shout "zero fees!" in big letters and quietly bake a 2% markup into the rate, and they'll still cost you more than a competitor charging a visible $5 fee with a near-perfect rate. We pull this comparison apart in markup vs transfer fee, and explain where the "real" rate comes from in the mid-market rate explained. For now, the lesson is: the rate is a fee in disguise. Treat it like one.

The lifting fee in the middle of nowhere

If you send through a bank wire, there's a second hidden cost lurking in the plumbing. International wires often hop through intermediary banks — correspondent banks — between your bank and your recipient's. Each one can deduct a charge in transit, frequently called a "lifting fee" or intermediary fee.

You don't see it. Your recipient often doesn't even know to expect it. They just receive less than you sent, with no clear explanation, because a bank somewhere in the middle skimmed $10–$20 off the top. On a transfer through two correspondent banks, that can happen twice. It's one of the main reasons bank wires quietly cost more than apps, which avoid the correspondent chain entirely — more on that in why banks give worse exchange rates.

The receiving-side charge

Even after the money lands in India, the recipient's bank can apply a fee for processing an inbound foreign remittance, especially on wire transfers. It might be a flat charge, or a small percentage. Whether this applies depends on the bank and the type of transfer, but it's a real cost that shows up on the recipient's end, not the sender's — which is exactly why the sender never notices it.

This is one reason transfer apps that promise "your recipient receives exactly X rupees" are clearer to budget around. With those, the landed amount is fixed and known. With a raw bank wire, the final figure can shrink between "sent" and "received" in ways nobody quoted you upfront.

The funding-method surcharge

Here's a self-inflicted one that catches people constantly. How you pay for the transfer changes the price. Most services charge more — sometimes a lot more — when you fund with a debit or credit card instead of a bank/ACH transfer.

Worse, your credit card issuer may treat the transfer as a cash advance, which carries its own fee (often 3%–5%) plus interest that starts accruing immediately, with no grace period. So a transfer that looked cheap in the app can pick up an extra layer of cost from your own card, completely outside the transfer service's pricing. Funding from a bank account is almost always cheaper, even though it's a day or two slower. If you're paying by card, check what your card treats the transaction as before you hit send.

The "promotional rate" that expires

Not a hidden fee exactly, but a hidden future cost. New customers often get a beautiful first-transfer rate or a waived fee. It's real, and it's a fine reason to try a service. The trap is choosing a long-term provider based on a one-time promo. After the first transfer, the rate reverts to normal, and "normal" might be worse than a competitor you skipped because their intro offer was less flashy. Judge a service by its ongoing rate, not its welcome gift.

The weekend and volatility spread

Currency markets close on weekends, but people still send money. To protect themselves from the rate moving while the market is shut, some services widen their margin on weekends and during volatile periods. You might get a slightly worse rate Saturday afternoon than you would have Tuesday morning, for no reason you can see. It's usually small, but on large transfers it adds up, and it's avoidable by sending during market hours when you can. The best time to convert USD to INR goes into timing in more detail.

The same trick, in a different costume: card spending in India

Once you can spot the rate markup in transfers, you'll start seeing it everywhere — and one place it bites NRIs constantly is using a US card while visiting India, or an Indian card while in the US. The mechanics are identical to a transfer's hidden markup.

When you swipe a US credit card in India, the conversion from rupees back to dollars on your statement carries a markup. Many cards add a foreign transaction fee of around 3% on top, and if the terminal offers to charge you "in dollars instead of rupees" — a feature called dynamic currency conversion — saying yes hands you a second, often worse, markup on top of that. The rule mirrors the transfer rule: always choose to be charged in the local currency (rupees, when you're in India) and let your own card do the conversion, and use a card with no foreign transaction fee if you travel often. Same hidden-markup game, different counter.

The reason this matters here is that it trains the instinct. The companies that hide costs in exchange rates do it in transfers, in card swipes, at airport currency kiosks, everywhere a conversion happens. The defense is always the same: find the real mid-market rate, and measure how far the deal you're offered sits from it.

A quick audit you can run on your last transfer

If you suspect a past transfer overcharged you, reconstruct it. Look up roughly what the mid-market rate was on the day you sent (historical rate charts are free online). Multiply your dollars by that rate to get the "perfect" rupees. Compare that against what actually landed. The difference is your total cost. Now subtract any fee you were charged — whatever's left is the hidden markup. Do this once with a bank wire and once with a good app, and the contrast usually settles which to use forever.

How to find the true cost in thirty seconds

Forget the fee. Forget the marketing. There's one number that captures every hidden cost at once: the rupees that actually land in India.

Here's the routine. Pick your amount — say $1,000. In each service you're comparing, enter that exact amount and the funding method you'll actually use, and read the figure it promises will be delivered in INR. That number already includes the markup, the fee, and (for apps that quote a guaranteed delivered amount) any receiving cost. Whichever service delivers the most rupees is the cheapest, full stop. It doesn't matter whether one calls its cost a "fee" and another hides it in the rate — the delivered total settles the argument.

For a bank wire, where the delivered amount isn't always guaranteed, mentally subtract a bit more for possible correspondent and receiving-side fees, then compare. The full arithmetic is in how much INR you'll receive after fees.

| Where the cost hides | How to catch it |

|---|---|

| Exchange rate markup | Compare delivered INR against the Google mid-market rate |

| Correspondent/lifting fee | Ask if it's a SWIFT wire; prefer apps that avoid the chain |

| Receiving-bank fee | Use services that guarantee the delivered amount |

| Card-funding surcharge | Fund from a bank account; check for cash-advance treatment |

| Expiring promo rate | Judge the ongoing rate, not the welcome offer |

| Weekend spread | Send during market hours when possible |

The mindset that protects you

The companies aren't necessarily villains — every business has to make money somewhere, and a transparent fee is a perfectly honest way to do it. The problem is asymmetry: a visible $5 fee feels worse than an invisible ₹2,800 markup, even though the markup costs far more, so marketing pushes everyone toward hiding the cost in the rate. Your defense is to refuse to play that game. Ignore what they call the cost. Look only at what lands. Once you train yourself to compare delivered rupees and nothing else, the hidden fees stop being hidden, because you're measuring the only number they can't fake.

For the bigger picture on choosing a service, see best ways to send money from USA to India, the full complete guide to sending money from the USA to India, and for a head-to-head on the major apps, Wise vs Remitly vs Xoom.

Why the markup hides best on large transfers

A closing point that's easy to miss: the bigger the transfer, the more the hidden markup costs you in absolute terms, and the more it pays to hunt it down. A 2% markup on $500 is about ₹860 — annoying, but small. The same 2% on $50,000 is roughly ₹86,000. The percentage didn't change; the stakes did. This is exactly why people sending large sums for a property purchase or moving years of savings home should treat the rate margin as the main event, not an afterthought. A careful comparison that saves a few rupees on a small transfer can save lakhs on a large one.

It's also why "no fee" marketing is most dangerous on big transfers. On a small send, a hidden markup and a visible fee are both small, so the choice barely matters. On a large send, choosing a low-markup service over a "no fee, high markup" one can be the difference of tens of thousands of rupees. The detail on this is in large money transfers to India, and the head-to-head math is in how much INR you'll receive after fees. Whatever the size, the defense never changes: ignore the labels, measure the delivered rupees against the mid-market rate, and pick the offer that lands the most.

Sources & further reading

- CFPB: Sending money to another country (remittance rights & disclosures)

- Federal Reserve: Foreign exchange rates (H.10 reference rates)

- CFPB: What is a cash advance and how does it work?

- FDIC Consumer News: Foreign transaction fees and dynamic currency conversion

- Reserve Bank of India: FAQs on remittances and inward remittance facilities

Frequently asked questions

What is an exchange rate markup? It's the gap between the real mid-market exchange rate and the worse rate a service actually gives you. The service keeps the difference. It functions as a fee but isn't labeled one, which is why it's the most commonly missed cost in a transfer.

Are "zero fee" transfers really free? Rarely. "Zero fee" usually means the cost has been moved into the exchange rate as a markup instead of charged as a fee. A zero-fee transfer with a 2% rate markup costs more than a $5-fee transfer at the real rate. Compare delivered rupees to know for sure.

What is a lifting fee? A lifting fee (or intermediary fee) is a charge taken by a correspondent bank that sits between your bank and the recipient's bank during a wire transfer. It's deducted in transit, so the recipient receives less than was sent, often with no clear explanation.

How do I find the true cost of a transfer? Enter your exact amount and real funding method into each service and compare the rupees actually delivered in India. That single figure captures the markup, fee, and receiving costs together. The service delivering the most rupees is cheapest, regardless of how each labels its charges.

General information, not financial advice. Fees, markups, and card-issuer policies change — confirm current details before transferring.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.