Why Banks Give Worse Exchange Rates Than Remittance Apps

How we produce this guide: we track live USD → INR pricing across major remittance providers, rank them by the rupees actually received after fees and exchange-rate margin (not the headline rate), and refresh figures as the market moves. See our full methodology.

Disclosure: this site shows ads and may, now or in future, earn a referral commission if you sign up with a provider through a link — at no extra cost to you. It never affects our rankings. See our terms & disclaimer.

Run a small test sometime. Ask your bank what rate it'll give you to convert $1,000 to rupees, then open a transfer app and check the same thing. The bank's number will almost always be worse — often by 1.5% to 3%, which on $1,000 is somewhere between ₹1,300 and ₹2,600 vanishing into thin air. Do that transfer monthly and the bank quietly pockets the cost of a decent dinner every year, on top of any wire fee you can actually see.

This isn't because your bank is uniquely greedy. It's structural. The way banks move money across borders is older, clunkier, and routed through more middlemen than a purpose-built transfer app, and every layer in that chain takes a cut. The fee on your statement is only the visible tip. The bigger cost is hidden in the exchange rate, and most people never realize it's there.

The fee you see vs the cost you don't

When you send an international wire, your bank shows you a fee — call it $30. That number feels like the cost of the transfer. It isn't. It's the smaller half.

The larger half is the exchange rate margin. Banks don't convert your dollars at the real market rate. They take the rate the world trades at, mark it down by a percent or three, and pass you the worse number. You never see "exchange margin: ₹1,800" on a receipt, because it's not charged as a fee — it's simply the rate you were given. Two costs, then: the wire fee you can see, and the rate margin you can't. The second one usually dwarfs the first.

A transfer app makes this comparison brutal for the bank. A service like Wise will show you the real mid-market rate and a small explicit fee, so you can see exactly what conversion cost. Put the two receipts side by side and the bank's "competitive" wire suddenly looks expensive. The mechanics of that hidden margin are covered in hidden fees in USD to INR transfers and the mid-market rate explained.

Why the bank's plumbing costs more

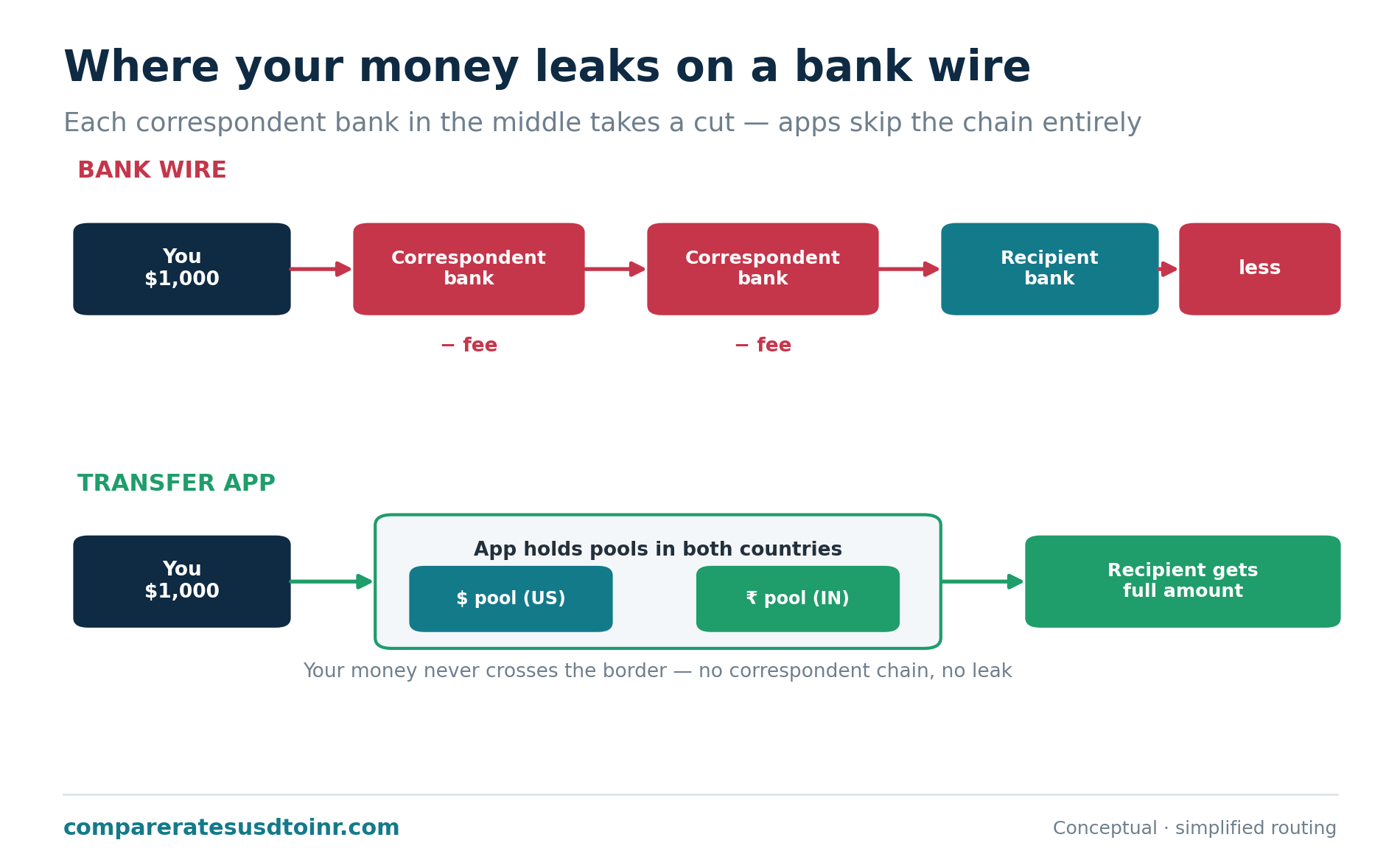

Here's the part most people never get told. When your bank sends dollars to India, it usually doesn't have a direct line to your recipient's bank. It hands the money through the SWIFT network, hopping across one or more correspondent banks — intermediary institutions that connect banks which don't have a direct relationship.

Each hop is a bank, and each bank can take a fee. There's often a "lifting fee" or intermediary charge somewhere in the chain that neither you nor your recipient agreed to explicitly, and it gets skimmed off in transit. Your recipient in India can end up receiving less than the amount you sent, with no clear explanation, because a correspondent bank in between took its slice. You sent $1,000; somewhere over the Atlantic, $15 evaporated.

Transfer apps mostly avoid this. They don't wire your individual dollars across the world. They hold pools of money in both countries — dollars in the US, rupees in India — and when you send, they pay out from their Indian pool locally while collecting your dollars in the US. Your money never actually crosses a border. That sidesteps the whole correspondent-bank chain, which is why apps are both cheaper and faster. No SWIFT hops, no surprise lifting fees, no three-day float.

Banks aren't built for small transfers

There's also a simple business reason. A bank's international wire system was designed for corporate treasury, large commercial payments, trade finance — moving serious money between institutions. Your $500 to your mother is an afterthought on that infrastructure, and it's priced like one. The bank has little incentive to compete hard on a retail remittance, because it isn't really their business; the rate margin is just easy money on a captive customer who didn't think to compare.

Transfer apps are the opposite. Personal remittances are their entire reason to exist. They've optimized relentlessly for exactly your transfer — small, personal, USD to INR — and they compete on rate because that's how they win customers from each other and from banks. When a company's whole business depends on giving you a good rate, you get a good rate.

"But my bank is safer"

This is the belief that keeps people overpaying, so it's worth confronting. The major transfer apps are licensed money transmitters, registered with FinCEN, regulated state by state, and they move tens of billions of dollars a year under serious oversight. Your money is not meaningfully less safe with a reputable app than with a bank wire. If anything, you get clearer tracking and a cleaner record.

The "safe" feeling around banks is mostly familiarity, not actual risk reduction. The genuine risks in any transfer — sending to the wrong account, falling for a scam — exist equally at a bank branch and in an app. Paying a 2.5% rate margin doesn't buy you safety. It buys the bank a margin.

A worked example, dollar for dollar

Numbers make this concrete. Suppose the real mid-market rate is ₹86.00 to the dollar, and you're sending $2,000 to family in India.

Through a transfer app with a 0.5% margin and a $6 fee, the recipient gets roughly (2000 − 6) × 85.57 ≈ ₹1,70,627. Through a bank wire, you might pay a $35 fee, get a rate marked down 2.5% to about ₹83.85, and then lose another $15 to a correspondent bank in transit. That works out to roughly (2000 − 35 − 15) × 83.85 ≈ ₹1,63,357. The bank route delivers about ₹7,270 less on the same $2,000 — and almost ₹6,000 of that gap is the rate margin and the correspondent fee, the parts you never see on the statement.

Send that monthly and the bank quietly costs you around ₹87,000 a year more than the app, for an identical transfer. That's not a rounding error. That's a meaningful chunk of the money you're trying to send home, disappearing into infrastructure and margin.

The pooled-money model, a little deeper

It's worth understanding why apps can avoid the correspondent chain, because it explains the whole cost difference. A transfer app keeps balances in both countries — a pool of dollars in the US, a pool of rupees in India. When you send $2,000, the app collects your dollars into its US pool and, separately, pays your recipient out of its Indian rupee pool. Your specific dollars never physically travel to India. The app just rebalances its pools periodically in bulk, at wholesale rates, far more cheaply than moving each customer's money individually across borders.

A bank, by contrast, genuinely pushes your individual payment through the international wire system, hop by hop, each hop a separate institution entitled to a fee. It's the difference between a local courier who already has parcels on both sides of the border and a single-package international shipment routed through three sorting hubs. Same destination, very different cost — and you pay for the routing.

When a bank wire actually makes sense

To be fair, the bank isn't always the wrong call. A few situations genuinely favor it.

For very large transfers — say, six figures for a property purchase — some banks will negotiate a better rate if you ask, especially if you're a priority or private-banking customer. Their margin on a huge sum can be tighter than their retail rate, and the per-transfer wire fee becomes trivial as a percentage. It's still worth comparing against a specialist, but the gap narrows. See large money transfers to India.

For transfers into your own NRE/NRO account, some Indian banks' dedicated remittance services (the bank's own arm, not a generic wire) are competitive and convenient, since they're built for exactly that flow. And if a recipient's bank or a specific corridor simply isn't supported by the apps, a wire may be your only route. But these are exceptions. For ordinary monthly support to family, the bank wire is the expensive habit, not the safe one.

How to stop overpaying

The fix is almost embarrassingly simple. Before any international transfer, check the actual rupees delivered through one or two transfer apps and compare against what your bank quotes for the same amount. Look at delivered INR, not the fee. If the app wins — and it usually will for ordinary amounts — use the app. If you're a private-banking client moving a large sum, ask your relationship manager for a negotiated rate and then compare that against a specialist before deciding.

That's the whole strategy. The reason banks keep their margin is that most people never run the comparison. They assume the bank is the default safe choice and never think to check, and the bank's pricing depends on exactly that assumption. The moment you actually compare delivered rupees, the choice usually makes itself, and you rarely go back.

It's worth saying plainly: none of this requires you to distrust your bank for the things banks are good at. Keep your accounts, your cards, your mortgage there. International remittance just happens to be a service banks price poorly and apps price well, because it's the apps' entire business and an afterthought for the bank. Using the right tool for this one job, while keeping everything else where it is, is simply matching each task to whoever does it best. For the full landscape of options, see best ways to send money from USA to India, and to compare costs properly, markup vs transfer fee.

What to do with this

The practical upshot ties into nearly every other decision about sending money home. If a bank wire is usually the expensive route, the natural next question is which route is cheapest for your situation — answered in best ways to send money from USA to India and the broader complete guide to sending money from the USA to India. To compare any two options honestly, you'll want the delivered-rupees math from how much INR you'll receive after fees, and to see exactly where the rate margin hides, hidden fees in USD to INR transfers.

There's one nuance worth holding onto. The bank's rate disadvantage shrinks as the amount grows, because a large transfer gives you leverage to negotiate and the per-wire fee becomes trivial as a percentage. So for a small monthly transfer, skip the bank without a second thought. For a very large one — a property purchase, say — get the bank's negotiated quote and compare it against a specialist before deciding, as covered in large money transfers to India. The rule isn't "banks are always wrong"; it's "banks are usually wrong for ordinary amounts, and you should always check rather than assume."

And once you've picked a route, the timing and rate-lock questions in best time to convert USD to INR and forward contracts and rate locks for NRIs help you avoid giving back your savings to a bad conversion moment.

Sources & further reading

- CFPB — Sending money internationally (consumer protections, exchange-rate & fee disclosures)

- CFPB — Regulation E, § 1005.30 remittance transfer definitions

- FinCEN — Money Services Business (MSB) definition, including money transmitters

- SWIFT — About us: how cross-border bank messaging works

- World Bank — Remittance Prices Worldwide (transfer cost and margin data)

Frequently asked questions

Why is my bank's exchange rate so bad? Banks mark down the real market rate by 1.5%–3% and pass you the worse number as the rate, in addition to any visible wire fee. They route transfers through SWIFT and correspondent banks that each take a cut, and retail remittances aren't a business they compete hard on.

Is a wire transfer to India cheaper than an app? Usually not, for ordinary personal amounts. Once you account for the rate margin and any correspondent-bank fees, a bank wire typically delivers fewer rupees than a transfer app. The exception can be very large transfers where a bank may negotiate a tighter rate.

What are correspondent bank fees? When banks don't have a direct relationship, payments hop through intermediary "correspondent" banks. Each can deduct a fee (sometimes called a lifting fee) in transit, which can leave your recipient with less than you sent and no clear line item explaining the shortfall.

Do banks charge a markup on currency conversion? Yes. Banks add a margin to the mid-market exchange rate on currency conversions. It isn't shown as a fee — it's simply built into the worse rate you're offered, which is why it's easy to miss.

General information, not financial advice. Rate margins and fees vary by bank and change over time — compare live quotes before transferring.

Figures in this article are illustrative examples to show how the math works — they are not live quotes and change daily. See the live USD → INR rates for current numbers, and always confirm the final amount on the provider’s own site before you send.